Most important takeaways…

- New federal loan caps limit NP students to $20,500 per year and $100,000 total starting July 2026.

- Nursing is excluded from the 11 professional degree categories that qualify for the higher $200,000 aggregate cap.

- A coalition of 24 states and D.C. filed a lawsuit on May 19, 2026, challenging the rule as unlawful.

- Existing undergraduate debt counts toward the $100,000 aggregate cap, shrinking available graduate borrowing even further.

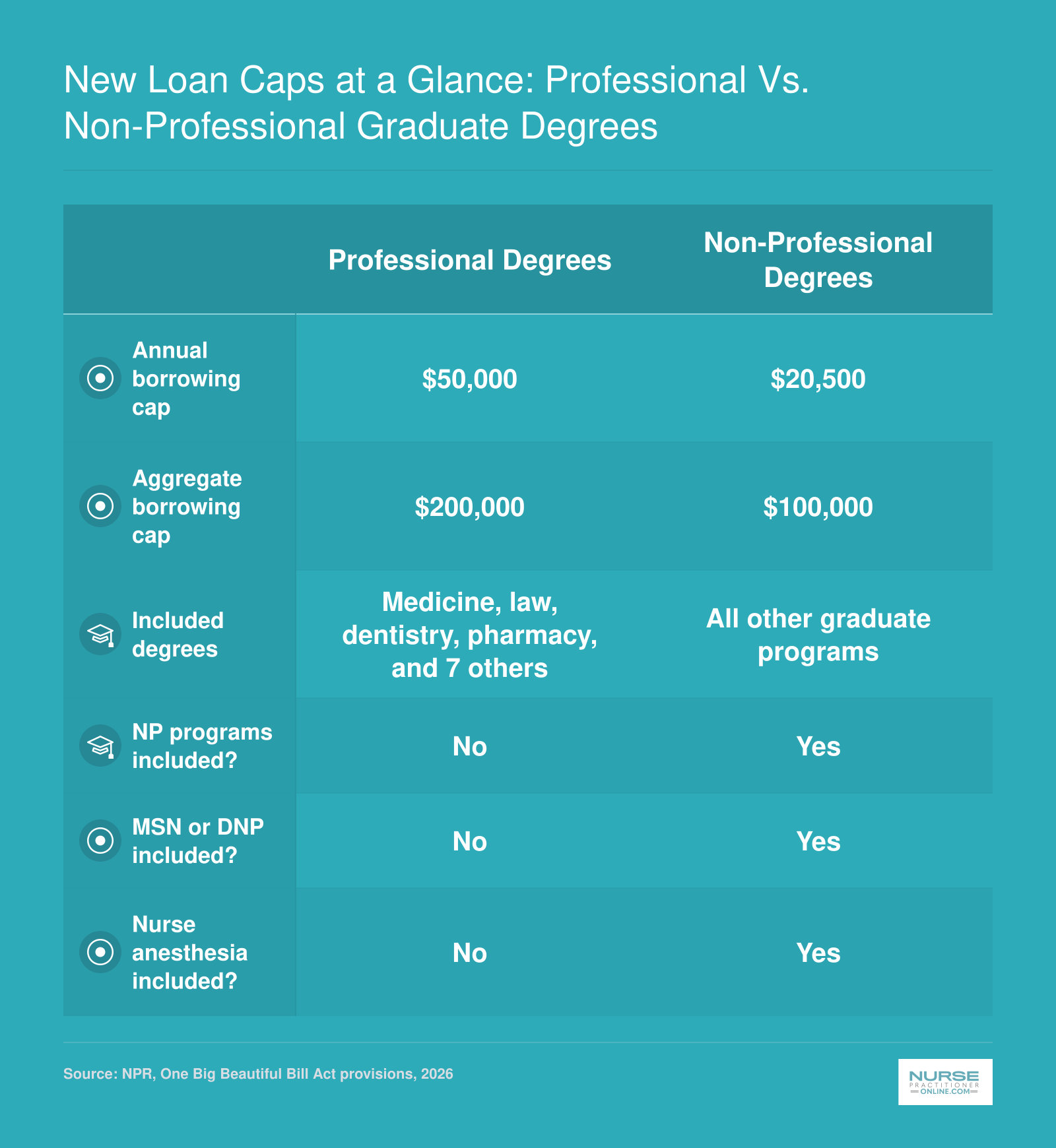

Starting July 1, 2026, federal graduate borrowing is capped at $20,500 per year and $100,000 total under the One Big Beautiful Bill Act, and nurse practitioner programs did not make the list of 11 exempted professional degrees that retain access to higher limits of $50,000 annually and $200,000 in aggregate.1

The exempted categories include chiropractic, dentistry, law, medicine, optometry, pharmacy, podiatry, and veterinary medicine, among others. Nursing, physical therapy, and nurse anesthesia were left out. For a nurse pursuing an MSN, DNP, or post-master's certificate in adult-gerontology, family practice, or psychiatric-mental health, the practical consequence is a real funding gap, pressure toward private loans at 7 to 13 percent, or, for some, walking away from advanced practice education altogether.

A 24-state lawsuit filed May 19, 2026 challenges the rule, but the caps take effect this summer regardless of how the courts move. Below, we break down what the new limits mean for your specific NP track, how existing undergraduate debt compounds the problem, and which funding strategies can help you close the gap.

What Changed: The New Federal Student Loan Limits Explained

Graduate student lending has been turned upside down. Beginning July 1, 2026, new federal student loan rules under the One Big Beautiful Bill Act introduce a two-tier borrowing system that sharply divides graduate students into those pursuing exempted professional degrees and everyone else.1 For the first time in decades, most graduate students, including future nurse practitioners, will face hard annual and aggregate caps on federal borrowing, while a narrow group of professional programs retains generous limits.

The Two-Tier System: Professional vs Non-Professional Graduate Degrees

Under the new rules, non-professional graduate degree programs (which include all nursing degrees) are capped at $20,500 per academic year and a total aggregate limit of $100,000 across undergraduate and graduate study combined.2 This aggregate cap includes any undergraduate borrowing, so an RN with $30,000 in prior loans would have just $70,000 available for graduate study.

In contrast, students enrolled in one of 11 exempted professional degree categories may borrow up to $50,000 per year with a total aggregate limit of $200,000.2 The exempted categories are:

- Chiropractic

- Clinical psychology

- Dentistry

- Law

- Medicine

- Optometry

- Osteopathic medicine

- Pharmacy

- Podiatry

- Theology

- Veterinary medicine

Nursing is conspicuously absent from this list. So are physical therapy, nurse anesthesia, and nearly every other allied health field. The Education Department drew the list from a regulation dating to the 1950s, long before advanced practice nursing existed in its modern form, and the One Big Beautiful Bill Act left that definition unchanged.

The Practical Math: A Funding Gap for DNP and MSN Students

Consider a typical Doctor of Nursing Practice program. A three-year DNP costs between $60,000 and $90,000 at many public universities, and over $120,000 at private institutions. If you are weighing the DNP vs PhD nursing decision, cost has always been a factor, but these new caps make it far more consequential. Under the old Grad PLUS system, students could borrow the full cost of attendance. Under the new caps, a student with no prior debt could borrow a maximum of $61,500 over three years ($20,500 times three). That leaves a gap of $20,000 to $60,000 or more.

For RNs carrying undergraduate loans, the math gets worse. A nurse with $40,000 in existing debt has only $60,000 of the $100,000 aggregate cap remaining. Over three years, that translates to roughly $20,000 per year, just under the annual cap, but any increase in undergraduate debt (interest capitalization, for example) could erode that headroom further. A two-year MSN program costing $50,000 total would require $30,000 to $40,000 out of pocket if prior undergraduate borrowing was substantial. Prospective students exploring affordable nurse practitioner programs will find that cost-conscious program selection matters more than ever.

Who Is Affected and When

The caps take effect July 1, 2026, for new borrowers. Students who had a Direct Loan disbursed for the same program at the same institution before July 1, 2026, and who remain continuously enrolled, are grandfathered under the old, more generous Grad PLUS rules for up to three years.3 After that grace period ends, or if they transfer programs or schools, the caps apply.

New borrowers are defined as students with no federal loans disbursed before July 1, 2026, or whose prior loans were paid in full before that date.3 In other words, if you begin an NP program in fall 2026 without any prior federal loans still in repayment, you are subject to the $20,500 annual and $100,000 aggregate caps immediately. If you were enrolled in spring 2026 and took a Direct Loan for that term, you may continue under the old system through spring 2029, provided you stay in the same program at the same school.

Students affected by these caps should also explore nurse practitioner loan forgiveness options that may help offset the increased out-of-pocket burden. These details come from guidance published by the U.S. Department of Education and clarified by the National Association of Student Financial Aid Administrators and the Pennsylvania Higher Education Assistance Agency.4 The 24-state lawsuit filed May 19, 2026, challenges the legality of the narrowed professional degree list, but as of today the caps remain scheduled to take effect on schedule.

New Loan Caps at a Glance: Professional Vs. Non-Professional Graduate Degrees

Under the One Big Beautiful Bill Act, federal student loan limits now split graduate programs into two tiers. The 11 degree categories classified as 'professional' receive significantly higher borrowing caps, while all other graduate programs, including nursing, physical therapy, and nurse anesthesia, fall into a lower tier with roughly 60% less borrowing power.

Why NP Programs Are Not on the 'Professional' Exemption List

When you compare who makes the cut for 'professional' loan treatment, chiropractors and podiatrists get earmarked for higher limits, while nurse practitioners, who deliver primary care every day in underserved areas, are left out. The disconnect is impossible to ignore.

The Origin of the 11-Category List

The list wasn't dreamed up in 2026. It's a relic from the 1950s, pulled from a regulatory definition the Education Department has left frozen for decades. Back then, advanced nursing practice was in its infancy, and federal regulations simply never caught up. Today's rule uses that dated list, unchanged, to decide which healthcare graduate students deserve more borrowing power. Understanding the history of nurse practitioners helps explain why a profession that barely existed in mid-century America was never added to a classification written in that era.

The Absurdity of Excluding Nursing

If you asked most patients who provides their primary care, they wouldn't draw a line between an NP and an MD. But under the new caps, chiropractic, podiatry, and clinical psychology all qualify for the higher professional-degree limits, while nurse practitioners, clinical nurse specialists, nurse midwives, and nurse anesthetists do not. The American Association of Colleges of Nursing has called this distinction indefensible, arguing it undervalues advanced practice nursing roles that are central to the healthcare system, especially in rural and low-income areas where nurse practitioners improve rural healthcare access.1

Will NP Programs Be Considered Professional Degrees?

As of June 2026, the straightforward answer is no. Unless the courts rule against the Education Department or Congress amends the law, NP programs are classified as general graduate programs for federal loans. This puts MSN, DNP, and post-master's certificate students under the $20,500 annual cap, with a $100,000 aggregate limit. For many, that won't come close to covering tuition and living costs. The 24-state lawsuit argues the rule illegally narrows the statutory definition of a professional degree, and if it succeeds, the list could be reopened. But no timeline is guaranteed, and students enrolling this year need to plan for the current limits.

The Debate: Broad Impact or Minor Problem?

The Education Department has pointed out that 80% of the nursing workforce does not hold a graduate degree, implying the caps affect only a slice of the field.1 But nursing advocates counter that this misses the point. Advanced practice nurses are the most educated segment of the profession, and their roles, particularly in primary care, mental health, and gerontology, are exactly where workforce shortages are most acute. Preston Cooper of the American Enterprise Institute argues the caps only bite "a small number of programs charging exorbitant prices."1 NP leaders strongly disagree, noting that even public university DNP programs can approach six figures when you factor in reduced work hours and clinical placement costs. The real issue is not exorbitant pricing; it's that federal loan structures haven't kept pace with the demands of modern healthcare education.

Questions to Ask Yourself

The 24-State Lawsuit: What It Means for NP Students

Waiting for a court to overturn the new caps versus planning for stricter loan limits starting July 2026 defines the dilemma facing prospective NP students this summer. On May 19, 2026, a coalition of 24 states and the District of Columbia filed suit in federal court against the U.S. Department of Education, arguing that the One Big Beautiful Bill Act's narrow definition of professional degrees violates both the Administrative Procedure Act and existing statutory authority.1 The lawsuit directly challenges the exclusion of nursing and other healthcare degrees from the $50,000 annual, $200,000 lifetime loan limits reserved for 11 favored fields. The coalition is seeking both injunctive relief and a declaratory judgment that the rule unlawfully narrows the long-standing federal definition of professional degrees.2

Current Status: No Court Action Yet

As of early June 2026, no preliminary injunction has been granted, no hearing dates have been set, and the Department of Justice has not yet filed a formal response on behalf of the Education Department.2 The lawsuit is in its earliest procedural phase. Absent emergency relief, the new caps will take effect for the 2026-2027 award year starting July 1, 2026. Students submitting FAFSA applications for fall 2026 enrollment are already operating under the assumption that the $20,500 annual graduate limit applies to MSN and DNP programs.

What the Lawsuit Could Change (and What It Won't)

If the coalition succeeds in obtaining a preliminary injunction, federal Grad PLUS loans could remain available to NP students temporarily while the legal challenge proceeds. That would restore the prior unlimited borrowing environment for students enrolled during the litigation window. If the lawsuit ultimately prevails on the merits, the Education Department would be compelled to either expand the exempted professional degree list to include nursing or abandon the narrowed definition altogether.

Conversely, if the court declines to enjoin the rule or if the lawsuit is dismissed, the caps stand. The lawsuit also does not address the underlying statutory framework of the One Big Beautiful Bill Act itself, only the Education Department's interpretation and implementation. Even a favorable ruling might not result in full restoration of unlimited borrowing if Congress does not amend the statute.

Impact on Rural Healthcare and Workforce Supply

American Nurses Association President Jennifer Mensik Kennedy stated that the rule "will be felt in real communities" and will harm rural healthcare access. The concern is not abstract. Many NP students already serve in underserved areas and rely on federal loans to bridge the gap between modest RN salaries and the cost of graduate education. With states that need nurse practitioners the most already struggling to recruit providers, restricting loan access now, when 80 percent of the nursing workforce lacks a graduate degree, risks compounding existing shortages.

Realistic Timeline: Months to Years, Not Weeks

Federal education litigation moves slowly. Even if a preliminary injunction hearing is scheduled this summer, a final judgment could take a year or more, and appeals could stretch the process into 2028. Students beginning programs in fall 2026 should not bank on a court rescue. Plan your financing as if the caps are permanent, and treat any favorable ruling as a bonus that might allow refinancing or additional borrowing mid-program. If you want to channel frustration into action, our nurse practitioner health policy toolkit outlines concrete steps for engaging your elected officials on issues like these. Relying on litigation as your primary funding strategy is a recipe for stalled enrollment and mid-program debt crises.

Impact by NP Track: MSN vs DNP, FNP vs PMHNP vs AGACNP

An MSN sits at one end of the spectrum, a BSN-to-DNP at the other, and the new $100,000 aggregate federal loan cap hits each path differently. The same cap that comfortably covers one program may fall short for another, and the gap widens further once you layer in specialty differences across FNP, PMHNP, and AGACNP tracks.

MSN vs DNP: The Length Multiplier

MSN programs generally run shorter and require fewer credits than DNP programs, so total tuition tends to land lower. For many students at public, in-state institutions, an MSN may still fit within the federal graduate cap, though fees, clinical placement costs, and books can push the real number higher than the sticker price suggests.

DNP programs, especially BSN-to-DNP pathways, demand more credits, more clinical hours, and more semesters. Understanding DNP entry-to-practice trends is important here because the profession is steadily moving toward doctoral preparation, making this funding gap even more consequential. At private universities, the total program cost can comfortably exceed the $100,000 aggregate limit on its own, which means students would need to close the gap with savings, employer support, scholarships, or private loans. Post-master's DNP students who already carried MSN debt face a compounding problem: their earlier graduate borrowing counts against the same lifetime cap.

Specialty Differences: FNP, PMHNP, AGACNP

Credit requirements vary by specialty, and so does the squeeze. If you are weighing primary care against acute care tracks, a comparison of AGNP vs FNP programs can help clarify the credit and clinical hour differences that drive cost.

- FNP: Often the most common track, with widely available programs at varied price points. Public, in-state options may stay within cap; private and out-of-state options frequently will not.

- PMHNP: Similar credit loads to FNP in many programs, but online and hybrid options can broaden affordable choices. Demand for psychiatric mental health providers is strong, which may justify higher investment if scholarships or loan repayment programs are accessible.

- AGACNP: Acute care tracks often require additional clinical intensity and specialized practicum sites, which can carry higher fees. Total cost tends to trend higher than primary care tracks at the same institution.

How to Model Your Own Gap

Do not rely on per-credit rates alone. To get an honest number:

- Pull the 2025-2026 tuition and fees page from each school you are considering, and look for total cost of attendance.

- Multiply per-credit tuition by the credits required for your specific track, then add mandatory fees, books, clinical placement charges, and technology fees.

- Use the school's net price calculator for a personalized estimate.

- Cross-reference expected salary ranges through the Bureau of Labor Statistics and program length norms through AANP and NONPF.

The cap is the same for everyone. The shortfall is not.

Related Articles

How the Caps Interact With Existing Undergraduate Debt

Most practicing nurses already carry significant federal student debt from their initial nursing education, and the new $100,000 aggregate cap applies across all undergraduate and graduate federal borrowing combined. This creates a far tighter squeeze than the headline numbers suggest. If you borrowed $40,000 to earn your BSN, you have only $60,000 in federal loan capacity remaining for graduate school, not the full $100,000. For many working RNs contemplating NP programs that cost $60,000 to $90,000 or more, the arithmetic simply does not work.

Understanding the Aggregate Limit Mechanic

The $100,000 cap is not a fresh allowance for graduate school. It is a lifetime ceiling on federal direct loans, including all subsidized and unsubsidized Stafford loans you have borrowed since your first degree. If your BSN required $35,000 in federal loans, the new rule leaves you with $65,000 of borrowing capacity. That may sound generous until you price out a Doctor of Nursing Practice program: tuition alone can run $70,000 to $90,000, and you still need to cover fees, clinical course charges, technology requirements, and living expenses if you reduce your hours at work. Understanding the difference between MSN and DNP pathways is important here, because program length and total cost vary significantly.

Private student loans do not count toward the federal aggregate limit, but they also do not help you if you are trying to maximize federal aid first. Many nurses already carry a mix of federal and private debt from their BSN years, and only the federal portion eats into the $100,000 cap.

A Realistic Scenario: The Funding Gap in Action

Consider an RN with $35,000 in existing federal student debt who enrolls in a $75,000 DNP program. Under the new caps, she has $65,000 of federal borrowing capacity remaining ($100,000 total cap minus $35,000 already borrowed). On paper, that sounds sufficient. In practice, she faces a $10,000 shortfall before accounting for fees, books, or the income loss from cutting back shifts to attend clinical rotations. If her program costs $80,000 all-in, the gap widens to $15,000, forcing her into private loans, employer tuition assistance, or out-of-pocket payment.

Does Paying Down Debt Free Up Capacity?

One critical unanswered question is whether paying down your existing federal loans restores borrowing capacity under the $100,000 cap, or whether the cap is based on the cumulative amount you have ever borrowed, regardless of repayment. As of June 2026, the Education Department has not issued clear guidance on this point. The safest assumption is that the cap reflects total lifetime borrowing, not current outstanding balance, but you should check your Federal Student Aid dashboard at studentaid.gov to see your aggregate loan history and consult your financial aid office before making enrollment decisions.

Why This Matters More for Nurses Than Other Graduate Students

This is the funding reality no other graduate student population faces quite so acutely. Unlike students entering law or medical school directly after a four-year degree, most NP students are working nurses who already used a substantial portion of their federal borrowing capacity to earn the BSN that qualified them for licensure in the first place. The new caps penalize that career ladder by treating all prior federal borrowing as a reduction in graduate school aid, leaving nurses with less room to fund advanced practice education than peers in fields that do not require an initial professional degree. If you are weighing your options, reviewing mistakes to avoid when enrolling in MSN program can help you make the most informed financial decisions before committing.

Alternative Funding Strategies for NP Students Under the New Limits

With federal graduate loan borrowing now capped at $20,500 per year and $100,000 in total, many NP students will face a funding gap that did not exist a year ago. The good news is that several federal programs, institutional scholarships, and employer benefits can help close that gap, sometimes dramatically. Here is what to explore before you sign a single promissory note.

HRSA Nurse Faculty Loan Program and Advanced Nursing Education Grants

The Health Resources and Services Administration (HRSA) administers two programs that are especially relevant right now. The Nurse Faculty Loan Program channels money through participating schools so that graduate nursing students can borrow at favorable terms, and up to 85 percent of the loan can be canceled if the graduate goes on to teach full time at an accredited nursing program. If you plan to teach after earning your degree, this is one of the most cost-effective paths available.

HRSA also funds Advanced Nursing Education grants, which flow to institutions rather than individual students. These grants support clinical training in primary care, behavioral health, and rural settings. While you cannot apply directly, choosing a school that holds one of these grants can translate into reduced tuition, funded preceptorships, or stipend support. Application windows for institutional grantees typically open in the spring for the following academic year, so ask your program director whether your school has applied for the 2026 to 2027 cycle.

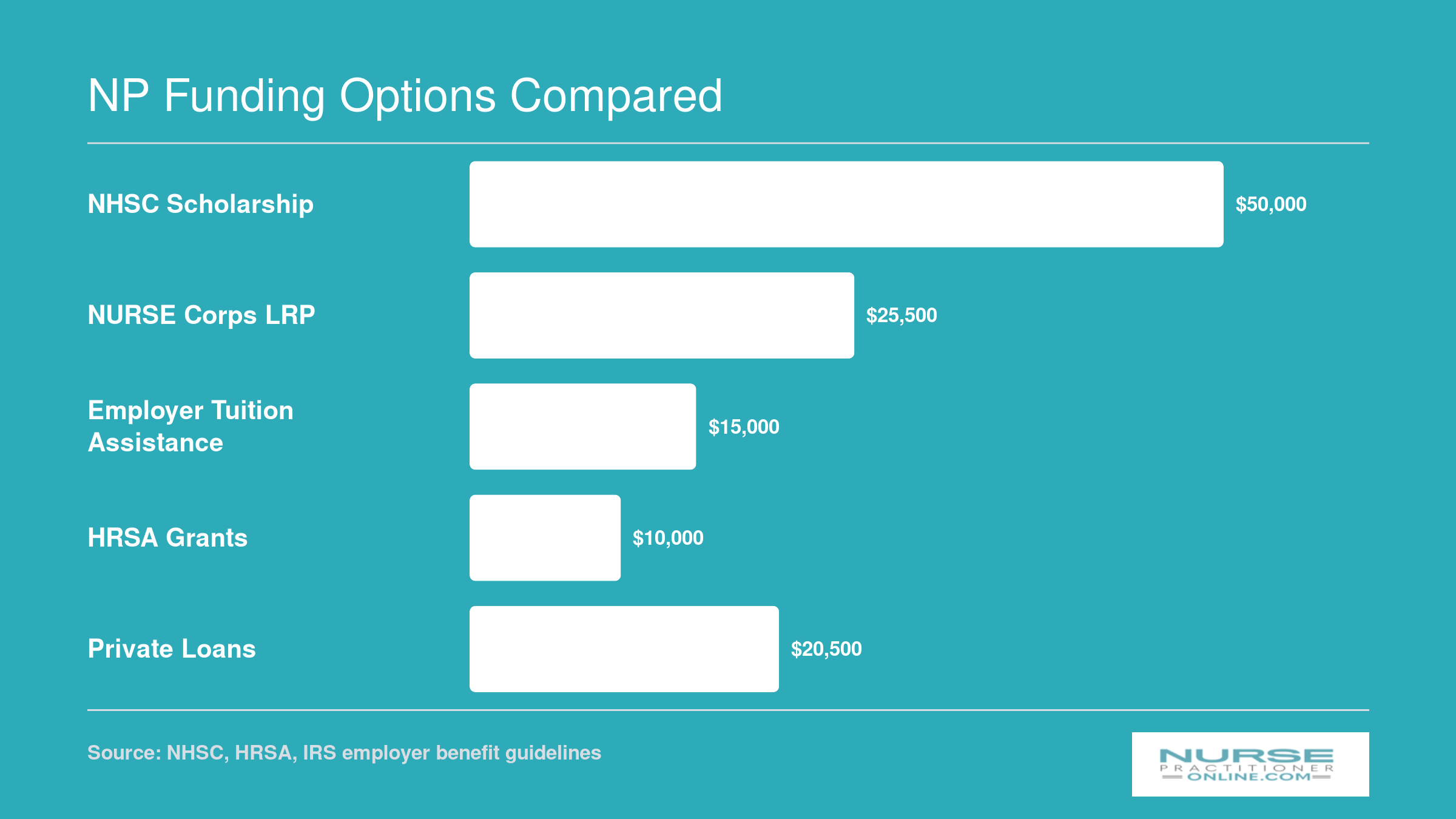

The NHSC Scholarship Program

The National Health Service Corps (NHSC) Scholarship Program remains one of the single most valuable awards an NP student can receive. It covers full tuition, required fees, and a monthly living stipend in exchange for a minimum two-year service commitment at an approved site in a Health Professional Shortage Area.1 The 2026 application cycle closed on May 8, so if you missed it, plan to apply as soon as the next window opens, typically in the early spring. Mark your calendar now: the NHSC awards are competitive, and deadlines are firm.

Because the service commitment places you in an underserved community, this program also positions you for additional downstream benefits like Public Service Loan Forgiveness on any remaining federal debt.

NURSE Corps Scholarship and Loan Repayment Programs

HRSA's NURSE Corps operates two tracks. The Scholarship Program covers full tuition, fees, and a monthly stipend in exchange for a two-year commitment at a Critical Shortage Facility.2 The 2026 scholarship application cycle has already closed, but the program reopens annually.

The NURSE Corps Loan Repayment Program is arguably even more relevant under the new caps. It repays up to 85 percent of qualifying nursing education loans for nurses who work at Critical Shortage Facilities: 60 percent after an initial two-year service term and an additional 25 percent for a third year. This program applies to both federal and private loans used for nursing education, which matters because students who are forced into private borrowing under the new limits can still benefit. Watch HRSA's website for the next application announcement, which typically posts in late winter or early spring.

Employer Tuition Assistance

Do not overlook the hospital or health system that already signs your paycheck. Many large employers offer tuition assistance ranging from $5,000 to $25,000 per year for nurses pursuing advanced degrees. Some systems, particularly those in rural or underserved markets, cover full NP tuition in exchange for a post-graduation service commitment of two to four years. If your employer does not advertise the benefit prominently, ask human resources directly. Even partial employer reimbursement can close much of the gap between the new $20,500 annual federal cap and actual program costs. If you are weighing different graduate pathways, comparing the is a DNP worth it question alongside your funding options can help you make a more informed decision.

Professional Scholarships Worth Pursuing

Several organizations offer scholarships specifically for NP students:

- AANP Scholarships: Awards of $2,500 to $5,000 with no service obligation, open to AANP member RNs. The 2026 deadline was March 18.3

- AANP Research Grants: Up to $10,000 for project-based work, also due March 18 for the current cycle.3

- WSOS NP Graduate Scholarship: A substantial $25,000 award spread over three years for students who commit to practicing in an underserved area of Washington state. The 2026 deadline was May 12.4

- Susan Peters NP Scholarship: A $2,000 award for NP students, offered through Samaritan Medical Center.5

These individual awards may seem modest against the cost of a full program, but stacking two or three of them alongside employer assistance and a federal program can make a meaningful difference.

Private Loans as a Last Resort

If a gap remains after exhausting every option above, private student loans can fill it, but they come with real trade-offs. Interest rates on private graduate loans are typically higher than federal rates and are often variable. You lose access to income-driven repayment plans, and private loans do not qualify for Public Service Loan Forgiveness. Borrow only what you truly need, compare offers from at least three lenders, and understand the full repayment terms before you sign. The American Association of Colleges of Nursing has warned that the new caps could push more nursing students toward these costlier products, so approach private borrowing with eyes wide open.

NP Funding Options Compared

Not all funding sources are created equal. The chart below compares the approximate annual dollar value of major NP funding options. Keep in mind that higher-value sources like the NHSC Scholarship and NURSE Corps Loan Repayment Program come with multi-year service commitments in underserved areas, while employer tuition assistance and HRSA grants have eligibility restrictions. Private loans can fill the gap but carry significantly higher interest rates and no forgiveness pathway.

Loan Forgiveness and Repayment Programs Still Available to NPs

For NPs weighing how to finance their graduate education under the new loan caps, the choice isn't just about borrowing less. It's about giving up access to some of the most valuable debt relief programs in healthcare. While the new limits may push you toward private loans to cover funding gaps, it's crucial to understand which forgiveness and repayment programs remain available to federal loan borrowers, and what you risk losing if you rely too heavily on private debt.

Public Service Loan Forgiveness (PSLF) Still Welcomes NPs

Public Service Loan Forgiveness remains one of the most powerful tools for advanced practice nurses. As long as you work full-time for a qualifying employer, such as a nonprofit hospital, a federally qualified health center (FQHC), or a government agency, you can have your remaining federal loan balance forgiven after 120 qualifying payments. Crucially, only federal Direct Loans count. Private loans, including any you take out to make up for the new cap shortfall, receive no forgiveness. This makes the shift toward private borrowing under the new limits doubly damaging: not only do you lose federal protections, but you also forfeit the chance for tax-free forgiveness that many NPs have counted on to manage six-figure education debt.

State-Level Loan Repayment Programs Offer a Steady Boost

Nearly every state runs a loan repayment program (LRP) aimed at recruiting nurse practitioners to underserved areas. These awards, often ranging from $10,000 to $50,000 in exchange for a service commitment, work alongside federal forgiveness; they are not mutually exclusive. Some states even structure their LRPs to complement PSLF, letting you use state funds to chip away at private loans while federal forgiveness handles the rest. If you're flexible about where you practice, state LRPs can fill a significant portion of the funding gap created by the new caps. Understanding which states need nurse practitioners the most can help you target locations with the most generous repayment incentives.

The Forgiveness Math Under Smaller Loan Balances

With annual graduate borrowing capped at $20,500, many NP students will graduate with much smaller federal loan balances than previous cohorts. At first glance, that means less debt to forgive. But it also means that the PSLF "windfall" shrinks proportionally: if you borrow only $60,000 rather than $150,000, you'll have a smaller amount forgiven after ten years of payments. The real danger lies in any private loans you take on. Those balances earn no forgiveness, accrue higher interest rates, and lack income-driven repayment options. In the worst case, a nurse could end up with a manageable federal balance but a crushing private loan burden that no program will erase. Choosing the most affordable nurse practitioner programs upfront is one of the best ways to minimize that private-loan exposure.

Income-Driven Repayment Plans: Still Here, but Under Review

For federal loans, income-driven repayment (IDR) plans remain available and cap your monthly payment at a percentage of your discretionary income. However, the future of the most generous plan, the Saving on a Valuable Education (SAVE) plan, is uncertain after multiple legal challenges. Even if SAVE is modified, other IDR plans like Pay As You Earn (PAYE) and Income-Based Repayment (IBR) will likely continue. Keep a close eye on policy updates, because whichever plan you're on directly affects both your monthly budget and the amount ultimately forgiven.

What Prospective NP Students Should Do Right Now

How can I prepare financially for NP school when federal loan rules are changing mid-stream? This is the urgent question facing thousands of nurses considering advanced practice education. Rather than waiting for clarity that may not come soon, prospective NP students should take concrete steps now to protect their educational plans regardless of how the legal and policy landscape unfolds.

Step 1: Calculate Your Remaining Federal Loan Capacity

Before making any program decisions, visit studentaid.gov and check your current federal loan balance. Under the new $100,000 aggregate cap for non-professional graduate degrees, any undergraduate federal debt you still carry counts against your total. If you borrowed $30,000 for your BSN, you would have only $70,000 in federal loan capacity remaining for your NP program. This calculation fundamentally shapes which programs remain financially viable for you without private loans.

Step 2: Reassess Program Length and Cost

The new caps may tilt the cost-benefit analysis toward shorter, less expensive programs. A public university MSN program costing $45,000 total looks very different under these rules than a private DNP program costing $120,000. This does not mean the DNP is no longer worth pursuing, but it does mean prospective students must weigh program prestige against financial reality more carefully than before. Compare tuition rates at public institutions in your state, examine hybrid versus fully online options, and consider whether an MSN with a later post-master's certificate might achieve your career goals at lower cost. If you are still exploring how to enroll in NP school online, start by narrowing your list to programs that fall within your remaining federal loan capacity.

Step 3: Pursue Non-Loan Funding Aggressively

Apply for every non-loan funding source before assuming you will need private loans. The National Health Service Corps scholarship and loan repayment programs, NURSE Corps, and HRSA grants all provide substantial funding for NP students willing to serve in underserved communities. Explore nurse practitioner loan repayment programs to understand your options for service-based forgiveness after graduation. Employer tuition assistance programs often cover a significant portion of graduate nursing education, and many hospitals have expanded these benefits to address workforce shortages. Professional nursing organizations offer scholarships specifically for advanced practice students. Exhaust these options first.

Step 4: Monitor the Lawsuit Without Building Your Plan Around It

The 24-state lawsuit challenging these loan limits could result in a preliminary injunction that temporarily restores Grad PLUS borrowing. However, building your entire financial plan around an uncertain legal outcome is risky. Check for updates from the American Association of Colleges of Nursing and major nursing news outlets, but develop a backup plan that assumes the caps remain in place. If the lawsuit succeeds, you will have more options. If it does not, you will already have a path forward.

Step 5: Make Your Voice Heard

Contact your members of Congress and let them know how these loan caps affect your ability to pursue NP education. The American Nurses Association and AACN are actively pushing for nursing to be added to the professional degree exemption list, and constituent pressure genuinely influences legislative priorities. Share your story with advocacy organizations, participate in their campaigns, and connect with other nursing students facing the same challenges. Policy changes rarely happen without sustained pressure from those affected.

Frequently Asked Questions About NP Student Loan Caps

The new federal student loan caps have raised urgent questions for nurses pursuing advanced practice degrees. Below are answers to the most common concerns, grounded in what we know as of June 2026.

- How much student debt does a typical nurse practitioner graduate with?

- Total debt varies widely by program type and institution, but NP graduates commonly carry between $40,000 and $120,000 or more in student loans. DNP graduates tend to owe more than MSN graduates because of additional credit requirements. Under the new $100,000 aggregate cap on non-professional graduate borrowing, some students may hit their federal limit before finishing, especially at higher-cost programs.

- Are NP programs classified as professional degrees under the new federal loan limits?

- No. Under the One Big Beautiful Bill Act, the 'professional degree' exemption is limited to 11 categories: chiropractic, clinical psychology, dentistry, law, medicine, optometry, osteopathic medicine, pharmacy, podiatry, theology, and veterinary medicine. Nursing, including all NP specialties, is excluded. That means NP students are subject to the lower cap of $20,500 per year and $100,000 in total graduate borrowing.

- Will current NP students be grandfathered under the old Grad PLUS loan limits?

- As of June 2026, the federal government has not confirmed a formal grandfathering provision for students already enrolled. The 24-state lawsuit may result in a temporary injunction that preserves current borrowing levels while the case proceeds. If you are currently enrolled or plan to enroll soon, contact your school's financial aid office for the latest guidance on how and when the caps take effect.

- How do the new student loan caps affect DNP vs MSN programs differently?

- DNP programs typically require more credits and clinical hours than MSN programs, which means higher total tuition. A DNP student is far more likely to hit the $100,000 aggregate cap before graduation. MSN students at moderately priced programs may stay within limits, but those at higher-cost institutions could still face a funding gap. Either way, the $20,500 annual cap creates year-by-year shortfalls for many students.

- What happens if the 24-state lawsuit succeeds?

- If the coalition of 24 states and the District of Columbia prevails, the court could block the new caps or require the Education Department to expand its definition of professional degrees. That could restore higher federal borrowing limits for NP and other healthcare graduate students. However, litigation can take months or years. In the short term, a preliminary injunction could pause the rule while the case moves forward.

- Can I still get PSLF if I have to take out private loans to cover my NP education?

- Public Service Loan Forgiveness applies only to federal Direct Loans, not private loans. If the new caps force you to borrow privately, those balances will not qualify for PSLF. Your federal loans would still be eligible as long as you meet the program requirements, including working full time for a qualifying employer and making 120 qualifying payments. Keeping your federal borrowing separate from private debt is important for tracking eligibility.

- Are there any bills in Congress to add nursing to the professional degree exemption list?

- As of June 2026, several lawmakers have publicly called for nursing to be added to the exempted list, but no standalone bill addressing this specific change has advanced through committee. The issue is gaining attention partly because of the lawsuit and advocacy from the American Nurses Association and the American Association of Colleges of Nursing. Prospective NP students should watch for legislative updates and consider contacting their representatives to support reclassification efforts.

The new federal loan caps are not hypothetical. Starting July 1, 2026, NP students face a $20,500 annual limit and $100,000 aggregate cap, with no exemption for nursing despite its central role in delivering primary care. The 24-state lawsuit offers hope, but its outcome remains uncertain and will not resolve quickly.

Do not wait for the courts. Calculate your total program cost now, factor in existing undergraduate debt, and pursue alternative funding aggressively through employer tuition assistance, NHSC scholarships, state loan repayment programs, and income-share agreements. Stay engaged in advocacy efforts through politics and nursing to reclassify NP degrees. For ongoing updates on the lawsuit, follow the original NPR coverage at npr.org.