Most important takeaways…

- Ten nursing organizations filed a lawsuit on May 29, 2026, challenging the DOE's professional degree exclusion.

- The rule caps NP student loans at $20,500 annually, while physicians and PAs borrow up to full cost.

- A DNP program priced at $80,000 could leave a funding gap over $39,000 without professional loan access.

Federal loan caps for graduate students are not just numbers on a website; they directly determine whether a working nurse can afford to earn a DNP or post-master's NP certificate. The Department of Education's final rule, effective this year, excludes advanced nursing degrees from the professional degree category, locking NP students into the standard $20,500 annual Direct Unsubsidized Loan limit.

On May 29, 2026, ten nursing organizations, including the ANA, ACNM, and NPWH, filed a lawsuit in Washington, D.C. to challenge that exclusion. Their argument is straightforward: advanced practice registered nurses complete clinical training comparable to other health professions that receive higher caps, and denying them equal borrowing power undermines the primary care pipeline.

The consequence for NP students is immediate. Campus-based DNP programs often cost $30,000 to $50,000 per year, meaning that even at maximum borrowing, a student faces a substantial out-of-pocket shortfall each year that no federal loan will cover. Whether you are weighing an MSN vs DNP, the financial calculus has shifted, and this lawsuit could shift it back.

What Happened: The Nurse Forward Lawsuit Explained

The debate over federal loan limits for advanced nursing education has shifted from policy discussion to federal litigation. On May 29, 2026, eleven national nursing organizations filed a joint lawsuit in the U.S. District Court for the District of Columbia.1 The case, widely referred to as the Nurse Forward lawsuit, directly challenges a Department of Education final rule that excludes post-baccalaureate nursing degrees from the "professional degree" designation used to set higher federal student loan borrowing limits.

The Filing and the Plaintiffs

The lawsuit was brought by a coalition that includes the American Nurses Association (ANA), American Association of Nurse Anesthesiology (AANA), Association of Women's Health, Obstetric and Neonatal Nurses (AWHONN), American College of Nurse-Midwives (ACNM), American Holistic Nurses Association (AHNA), Association of Pediatric Hematology/Oncology Nurses (APHON), Chi Eta Phi Sorority, Incorporated, Health Ministries Association (HMA), National Association of Clinical Nurse Specialists (NACNS), National Association of Nurse Practitioners in Women's Health (NPWH), and the American Association of Nurse Attorneys. Together, these groups represent hundreds of thousands of nurses, including nurse practitioners, clinical nurse specialists, nurse anesthetists, and nurse-midwives.

What the Final Rule Means for NP Students

The Department of Education rule, part of updated federal loan regulations, redefines which graduate programs qualify as a "professional degree" for purposes of Grad PLUS and unsubsidized loan limits. Previously, many advanced practice nursing programs (whether DNP vs PhD nursing or MSN tracks) were treated similarly to medicine, law, and other professional fields, allowing students to borrow up to the full cost of attendance minus other financial aid. Under the new rule, however, the Department explicitly lists only certain health professions, such as physicians, dentists, and physician assistants, as eligible for the highest federal graduate loan caps. Advanced nursing degrees are now categorized separately, effectively capping borrowing at the standard graduate level, which can leave a significant gap between tuition and available federal loans.

How This Lawsuit Differs from Other Legal Challenges

Nurse Forward is not the only court action against the Department's professional-degree rule. In late May 2026, a parallel lawsuit was filed in the U.S. District Court for the District of Maryland by 24 state attorneys general, the District of Columbia, and the governors of Kentucky and Pennsylvania.2 That multistate challenge focuses on broader consumer-protection and workforce arguments. The Nurse Forward case, in contrast, is led by nursing organizations that can speak directly to the financial and educational impact on current and future NPs. Both lawsuits target the same rule, but the nursing coalition's standing as directly affected parties gives it a distinct tactical footing. As of June 2026, neither case has seen substantive rulings, and both remain in early stages.

The Case's Core Argument

The plaintiffs argue that the Department of Education ignored clear statutory language that allows post-baccalaureate professional programs to be included under the higher loan limits. They contend that advanced nursing education, whether leading to a DNP, MSN, or PhD in nursing, demands at least the same rigor, clinical hours, and societal necessity as the listed professions. By excluding nursing, the rule creates an arbitrary financial barrier, discouraging nurses from pursuing graduate credentials just as severe workforce shortages emerge in adult-gerontology primary care, behavioral health, and rural medicine. The coalition's press release underscores that the rule "disregards the essential role" of these nurses in the U.S. healthcare system.1 For NPs weighing whether to pursue doctoral education, this lawsuit could reshape the financial calculus, and understanding whether a DNP is worth it may depend in part on its outcome.

What Is a 'Professional Degree' and Why Does It Matter for NPs?

In federal student aid language, a 'professional degree' is not about prestige or rigor. It is a specific regulatory label that unlocks higher borrowing limits for students in designated programs. The Department of Education (DOE) defines this category through a fixed list of 11 fields, including medicine, dentistry, law, and clinical psychology.1 Programs on that list qualify for annual and aggregate federal loan caps far above those available to ordinary graduate students.

The Department's Criteria and the 11 Chosen Fields

The statutory definition requires a program to provide clinical training, prepare graduates for licensure, and serve as the terminal practice credential for the profession. The 11 fields designated in the final rule (MD, DO, DDS, DPM, DC, OD, PharmD, DVM, JD, theology, and clinical psychology) meet these criteria by offering extensive supervised practice and leading directly to a license required for independent practice.2 Qualifying students can borrow up to $50,000 per year and $200,000 over their degree.3

Why Nursing Was Left Out

Despite DNP, MSN-NP, and even PhD nursing programs all involving clinical hours, licensure preparation, and terminal practice credentials, the DOE's April 30, 2026 final rule (effective July 1, 2026) categorizes them as ordinary graduate programs.4 The agency used a program-based list, not a function-based test, and did not alter the list from its initial proposal.2 The nursing organizations suing the DOE argue that advanced nursing degrees indisputably meet the same statutory requirements, and that the exclusion is arbitrary and damaging. If you are weighing the costs and career outcomes of these paths, our comparison of MSN vs DNP breaks down the key differences.

The Dollar Difference: Loan Caps That Hit NP Students Hard

The concrete financial impact is immediate. Under the new rule, graduate students outside the 11 designated fields, including all MSN, DNP, and post-master's NP certificate students, face these caps: - Annual limit: $20,500 (versus $50,000 for professional students) - Aggregate (lifetime) limit: $100,000 (versus $200,000 for professional students)

With many DNP programs costing over $80,000 in total, and some private programs exceeding $120,000, the lower aggregate cap alone may leave a significant funding gap. Roughly 95% of graduate nursing students currently borrow below the annual limit, but a shift to more expensive programs or longer degree paths could push many against the new ceilings.3

How the Caps Apply to Different Nursing Paths

The DOE rule treats all post-baccalaureate nursing programs identically as non-professional graduate study.5 That means: - MSN-NP programs: The $20,500 annual and $100,000 aggregate caps apply. - DNP programs: Same lower caps, even though the DNP is the terminal clinical doctorate. For nurses wondering whether the doctor of nursing practice (DNP) still makes financial sense, the tighter loan limits add a new dimension to the calculation. - Post-master's NP certificates: Also capped at $20,500/$100,000, which can be especially problematic because certificate students often have existing graduate debt from a previous MSN or DNP.

Questions to Ask Yourself

How the New Loan Caps Affect NP Students: A Tuition-Vs.-Cap Reality Check

Will the $20,500 annual federal loan cap actually cover my nurse practitioner program?

The funding gap for campus-based DNP programs

When the Department of Education excludes advanced nursing degrees from the professional loan designation, the standard graduate student borrowing limit applies: $20,500 per year in Federal Direct Unsubsidized Loans, with an aggregate cap of $138,500. For most campus-based DNP programs, that simply does not come close. National averages now put DNP tuition between $28,000 and $43,000 per year, with cost of attendance at private non-profit doctoral programs surpassing $44,770.2 At Duke University, the per-credit rate is $2,250, meaning a full-time student can easily face over $50,000 in annual tuition alone.3 Touro University California's ADN-to-MSN track reports an annual cost of attendance of $50,734.4 A $20,500 loan leaves a gap of $30,000 or more, year after year. Even with federal work-study or modest scholarships, students are either forced to borrow high-interest private loans, drain savings, or delay enrollment.

Where online and public programs offer a tighter fit

Some pathways do stay closer to federal limits, though the margin remains tight. Spring Arbor University's online MSN lists a total program cost of $39,850.5 Spread over two or three years, the annual tuition sits below the $20,500 cap, making the Direct Unsubsidized Loan almost sufficient for tuition, but not for living expenses if you borrow for the full cost of attendance. Public university MSN tracks, with average annual tuition around $10,150 to $12,480, may fit comfortably for tuition, yet even those total costs of attendance at public graduate programs ($25,460) exceed the annual loan limit. Online delivery often trims housing and commuting costs, and comparing online vs on-campus NP programs can help you estimate the real savings. Clinical hours still demand on-site presence, however, and those travel and lodging expenses add up.

The hidden cost of relying on private loans

When the federal loan cap is exhausted, students turn to private educational loans or Graduate PLUS Loans. Grad PLUS loans can cover the gap but carry higher origination fees and interest rates than Direct Unsubsidized Loans, and they require a credit check that not every nurse practitioner student, especially those carrying prior degree debt, will pass. Private loans typically lack income-driven repayment options or Public Service Loan Forgiveness eligibility, leaving borrowers more vulnerable after graduation. If you are already weighing how to manage debt long-term, exploring nurse practitioner loan forgiveness options now is a smart move.

Calculate your own gap

Because program costs vary dramatically by state, format, and specialization, plugging in your school's published cost of attendance is essential. Start with the annual total, subtract the $20,500 Direct Loan maximum, and then subtract any grants or scholarships. The remainder is your real annual funding gap. If your program spans three years for a DNP, multiply that number by three. Recognizing that gap early lets you explore institutional aid, Nurse Corps loan repayment programs, and employer tuition benefits before the pressure of tuition bills mounts.

NP Vs. PA Vs. MD Vs. Other Health Professions: Loan Limit Comparison

Two professional trajectories, similar clinical intensity, but a single policy distinction can widen or narrow a student's borrowing power by tens of thousands of dollars. The Department of Education's 2026 rule on professional degree designations creates that divide, and for nurse practitioners, it lands squarely on the low side.1

Understanding Professional Degree Status

The federal graduate loan system splits programs into two tiers. "Professional degree" programs qualify for higher annual and lifetime unsubsidized borrowing limits because the government recognizes their length, rigor, and essential role in producing licensed practitioners. Programs not labeled as professional fall into the general graduate category with far tighter caps.

Federal Loan Caps by Profession

The gap is stark when you line up health professions side by side:1

- MD/DO: Professional degree. Annual unsubsidized cap of $50,000, with an aggregate lifetime limit of $200,000.2

- PharmD: Professional degree. Same $50,000 annual and $200,000 lifetime caps.

- NP (DNP/MSN): Not professional. Annual cap sits at $20,500, and the lifetime aggregate maxes out at $100,000.

- PA: Not professional. Identical to NP: $20,500 annually and $100,000 lifetime.

- Doctor of Physical Therapy (DPT): Not professional. Same $20,500/$100,000 limits, though total program costs routinely reach $108,000 to $126,000.

The Clinical Training Gap in Loan Policy

The lawsuit filed in May 2026 argues that the exclusion of advanced nursing degrees from the professional category defies both statute and common sense. Whether you are weighing DNP prerequisites or mapping out a multi-year plan, the financial picture matters early. NP programs demand hundreds of clinical hours, mirroring the intensity and length of programs that do receive professional designation. Yet a DNP or MSN-prepared NP faces a borrowing ceiling barely half that of a pharmacy or medical student.1 This financial wall hits hardest for students in high-tuition specialties like adult-gerontology, where full-time work during clinical semesters becomes nearly impossible.

The mismatch doesn't just affect individual students. It constricts the entire pipeline of advanced practice clinicians at a moment when demand for primary and specialty care is surging.

Who Filed the Lawsuit and What Are They Arguing?

The Nurse Forward lawsuit is a coordinated legal action filed by ten influential nursing organizations against the U.S. Department of Education. The suit challenges a final rule that excludes post-baccalaureate nursing degrees from the definition of a "professional degree," a designation that determines how much federal student loan money a graduate student can borrow. By keeping advanced nursing out of this category, the rule imposes lower borrowing caps on NP, DNP, and other graduate nursing students, potentially making advanced education financially out of reach for many.

The Coalition Behind Nurse Forward

The breadth of the plaintiff groups underscores how deeply this policy affects the entire nursing profession. The coalition includes:

- American Nurses Association (ANA): The nation's largest nursing organization, representing registered nurses across all specialties.

- American Association of Nurse Anesthesiology (AANA): The voice for certified registered nurse anesthetists, an advanced practice role requiring a doctoral-level education.

- Association of Women's Health, Obstetric and Neonatal Nurses (AWHONN): Dedicated to advancing the health of women and newborns, with many members pursuing graduate degrees.

- American College of Nurse-Midwives (ACNM): Representing certified nurse-midwives, who often hold master's or doctoral degrees.

- American Holistic Nurses Association (AHNA): Supporting nurses who integrate complementary and alternative therapies into practice.

- Association of Pediatric Hematology/Oncology Nurses (APHON): Focused on specialized pediatric cancer and blood disorder nursing.

- Chi Eta Phi Sorority, Inc.: A historically Black professional nursing sorority with a long history of community service and advocacy.

- Hispanic Medical Association (HMA): An organization serving Hispanic nursing and healthcare communities.

- National Association of Clinical Nurse Specialists (NACNS): Advancing the clinical nurse specialist role, a graduate-prepared advanced practice registered nurse.

- Nurse Practitioners in Women's Health (NPWH): Representing nurse practitioners who specialize in women's health, many of whom hold doctoral degrees.

This coalition pulls together general nursing advocacy, specialty APRN groups, and organizations that represent underrepresented racial and ethnic communities within nursing, showcasing a unified front that the rule harms nurses across all facets of care.

Core Legal Arguments: Misapplied Definitions and Arbitrary Exclusion

At the heart of the lawsuit is the claim that the Department of Education misread the statutory definition of a professional degree.1 The Higher Education Act sets higher loan limits for students in "professional degree programs," traditionally including fields like medicine (MD), dentistry (DDS), and physician assistant (PA) studies. The plaintiffs argue that advanced nursing degrees, such as the MSN, DNP, and PhD in nursing, meet the same statutory criteria: they require a prior bachelor's degree, lead to clinical licensure or advanced certification, and are essential for entry into advanced practice. The Department's final rule, they say, arbitrarily wrote nursing out of that definition without justification.

The organizations also contend that the Department ignored substantial public comments that detailed how advanced nursing education is clinically rigorous, heavily regulated, and directly comparable to other health professions that remain eligible for higher loan limits. They accuse the Department of acting arbitrarily and capriciously, a violation of the Administrative Procedure Act, by excluding programs that produce nurse practitioners, nurse anesthetists, nurse-midwives, and clinical nurse specialists, all of whom deliver care that often overlaps with that of physicians and PAs. For nurses interested in shaping policy outcomes like this one, building advocacy skills through a nurse practitioner health policy toolkit can make a real difference.

A Different Path from the Attorneys General Challenge

It's important to distinguish this lawsuit from the separate legal challenge being pursued by a coalition of state attorneys general. The multistate AG lawsuit may focus on federalism concerns, arguing the rule infringes on state authority to define and regulate nursing practice and education. In contrast, the Nurse Forward case is built directly on statutory interpretation and the arbitrary-and-capricious standard. The nursing organizations are not arguing about states' rights; they are arguing that the Department simply got the law wrong and failed to follow proper rulemaking procedures.

Why Workforce Shortages Are Central to the Case

The plaintiffs underscore a practical consequence: by creating financial barriers to graduate nursing education, the rule will worsen existing workforce shortages. Nurse practitioners and other advanced practice nurses are often the primary care providers in rural and underserved communities. If loan caps force nurses to abandon or delay their education, the pipeline of new providers shrinks exactly where they are needed most. The lawsuit explicitly ties the financial exclusion to a looming public health crisis, arguing that the Department's action undermines the nation's healthcare workforce at a critical time.

Possible Outcomes: What Happens if NPs Win or Lose?

For nurses weighing a return to school this year, the lawsuit injects both hope and hard choices. You are balancing the promise of a DNP or post-master's certificate against borrowing limits that may leave a significant tuition gap. The legal battle could reshape that equation, but it will not resolve quickly. Understanding the range of possible outcomes helps you plan with eyes open.

If the Courts Side with Nursing Organizations

The most favorable scenario starts with a preliminary injunction. A federal judge could block the Department of Education (DOE) rule before it takes effect, temporarily preserving the higher professional degree loan limits while the case moves ahead. This would give NP students enrolling in Fall 2026 or Spring 2027 the same borrowing capacity they expected before the rule change. Then, if the court ultimately rules that the DOE arbitrarily excluded advanced nursing degrees, it could vacate the rule entirely. That would permanently restore access to up to $20,500 in unsubsidized loans and Grad PLUS eligibility up to the cost of attendance, putting DNP, PhD, and post-master's NP programs back on equal footing with law, medicine, and other professional degrees. In the best case, a final ruling could also prompt the DOE to revise its definition through proper notice-and-comment rulemaking, locking in parity for future cohorts.

If the Department of Education Rule Stands

A loss would mean the DOE's final rule, and its reduced loan caps, endures. Post-baccalaureate nursing students would continue to face the lower graduate borrowing limits, which may not cover full program costs at many institutions. The immediate effect would be forcing some students to delay or abandon enrollment, particularly those who cannot bridge the gap with employer tuition assistance, private loans, or personal savings. Schools may respond by restructuring tuition, expanding payment plans, or seeking institutional aid, but these adjustments take time. In the longer term, the profession could see a chilling effect on advanced practice enrollment, just as demand for primary care, gerontology, and mental health services intensifies in the states with most need for nurse practitioners.

Potential Compromises and Political Paths

Courts do not always issue all-or-nothing rulings. A judge might grant partial relief, for instance carving out DNP programs that include a clinical residency, while leaving other post-baccalaureate nursing degrees under the lower caps. Alternatively, the court could stay the rule pending appeal without a preliminary injunction, leaving students in limbo. Beyond the courtroom, Congress could step in. Bipartisan pressure to address healthcare workforce shortages might lead to legislative changes that explicitly include advanced nursing degrees in the professional degree definition. The DOE could also voluntarily revisit the rule under a new administration or sustained political pressure, avoiding a lengthy appeals process.

The Timeline Reality for Enrolling Students

Even if the lawsuit succeeds quickly, appeals could stretch the timeline to a year or more. Students starting programs in Fall 2026 should not bank on a favorable ruling to arrive before tuition bills come due. That means building a contingency plan now: identify non-federal funding sources, speak with financial aid offices about estimated costs under both scenarios, and consider whether a phased enrollment plan makes sense. If you are still deciding on a program format, our comparison of how long a DNP program takes can help you weigh accelerated vs. part-time timelines against financial uncertainty. Nurse practitioner candidates who wait for the legal dust to settle may risk losing a semester or a year of earnings, so the decision to defer has its own price tag.

It is also worth watching the separate lawsuit filed by a coalition of state attorneys general. That case could independently block the rule or create a circuit split that accelerates Supreme Court review, potentially widening or narrowing the options for NP students. For now, staying informed and preparing for multiple paths is the practical strategy.

NP Workforce Shortages: Why This Lawsuit Matters Beyond Student Loans

At its core, this lawsuit is about whether the U.S. will have enough nurse practitioners to meet patient demand in the coming decade. While the immediate fight is over loan limits, the real stakes are the communities that depend on NP care, especially older adults, people with mental health needs, and those living in rural areas.

The Numbers Behind the Need

Current federal data paints a complex picture. HRSA projects a national surplus of about 56,990 NP FTEs by 2026, driven by rapid growth in NP programs.1 However, that aggregate number masks severe geographic and specialty mismatches. For example, 92 million Americans already live in primary care Health Professional Shortage Areas (HPSAs), where access to a primary care provider is limited.2 In California alone, HRSA models a 22% NP shortage by 2038.3 The same pattern holds for behavioral health: the demand for psychiatric-mental health NPs far outstrips supply, even when the national NP count looks adequate on paper. These geographic disparities are explored in detail in our look at nurse practitioners in rural healthcare.

What Happens When the Pipeline Slows

The Department of Education's current rule classifies post-baccalaureate nursing degrees, including MSN, DNP, and PhD programs, as graduate rather than professional degrees. That slashes federal borrowing limits, making NP education less affordable for many working nurses. If enrollment drops, the downstream effect is straightforward: fewer new NPs graduate each year. The populations hit hardest will be those who already lean most heavily on advanced practice nurses: adults over 65 managing multiple chronic conditions, people in rural communities with few other providers, and individuals seeking mental health care amid a deepening behavioral health crisis. Non-metro areas already face a projected 24% registered nurse shortage by 2028, compared to just 5% in metro areas.3

Specialty Shortages That Could Worsen

Two specialties face especially acute risk. Adult-gerontology nurse practitioners are the backbone of care for America's rapidly aging population, a demographic that is projected to keep growing. Psychiatric-mental health nurse practitioners, meanwhile, are on the front lines of a mental health epidemic, with demand far outpacing the number of trained professionals. Understanding the NP role in modern healthcare helps illustrate why restricting the pipeline into these specialties would be especially damaging. If financial barriers shrink the NP pipeline, these specialty shortages will intensify, leaving vulnerable patients with longer wait times or no care at all.

The Organizations' Workforce Argument

The ten nursing organizations that filed the lawsuit explicitly raised workforce impact as a core concern. They argue that the rule "ignores the essential role of advanced practice and graduate-prepared nurses" and creates financial obstacles that will discourage enrollment precisely when U.S. healthcare needs more advanced practitioners. This isn't just about student borrowing; it's about whether the healthcare system will have the clinicians it needs to serve an increasingly complex patient population in the years ahead.

In 2023, there were 385,000 licensed nurse practitioners in the United States, with the workforce growing at an annual rate of 8.5%. That pace far outstrips many other health professions, underscoring the rising demand for NP care.

Practical Steps for NP Students Right Now

Every NP student should run a personal funding gap calculation immediately. Postponing this step could mean a mid-program financial crisis. The Department of Education's final rule, challenged by the Nurse Forward lawsuit, caps annual Direct Unsubsidized Loan borrowing for non-professional graduate degrees at $20,500, far below what many NP programs cost. Until a court intervenes, you need a clear-eyed plan.

Calculate Your Personal Funding Gap

Pull your program's published cost of attendance for the 2026-2027 academic year. Include tuition, fees, books, and estimated living expenses if you plan to use loans for support. Subtract the $20,500 annual federal loan cap. If you have access to Direct PLUS Loans (available to graduate students, though with higher rates and a credit check), you can borrow up to the cost of attendance minus other aid, but PLUS Loans are not capped by the professional degree rule. The immediate concern is that many NP students rely first on the more favorable Direct Unsubsidized Loan because of lower origination fees and interest rates; the cap forces earlier, heavier PLUS reliance. The key number is your residual need after federal loans and any grants or scholarships you already hold. Write that number down. It represents your real funding gap.

Explore Alternative and Supplemental Funding

- Employer tuition reimbursement: Many hospitals and health systems offer annual tuition benefits ranging from $3,000 to $10,000. Confirm whether your employer's program covers DNP or MSN coursework and whether it requires a post-graduation service commitment.

- State nursing workforce grants: More than 30 states administer loan repayment or scholarship programs for advanced practice nurses. Check your state board of nursing website for current cycles; deadlines often fall in early fall.

- HRSA Nurse Corps Loan Repayment Program: This federal program pays up to 85% of qualified student loans for NPs who work in designated Health Professional Shortage Areas after graduation. It is separate from the loan cap issue and remains fully available.

- Institutional scholarships: Many NP programs have dedicated scholarship funds that go unawarded because students don't ask. Schedule a conversation with your program's scholarship coordinator.

- Private loans as a last resort: Interest rates are typically higher and variable, and repayment terms are less flexible. Exhaust all federal options first.

Importantly, Public Service Loan Forgiveness eligibility is unchanged by the borrowing caps. PSLF cares only about your employer type and qualified repayment plan during the 120-payment period, not about how much you borrowed or under which loan program. The caps simply alter how much you can access initially; they do not touch PSLF.

Consider Enrollment Timing, But Don't Bank on It

If the lawsuit secures a preliminary injunction before the fall 2026 semester, the previous higher caps ($20,500 with additional Grad PLUS availability up to the full cost of attendance) could be temporarily restored. However, legal timelines are unpredictable. Plan your fall finances assuming the new caps stand. If the injunction comes through, treat it as a welcome relief, not as Plan A.

Contact Your Financial Aid Office Now

Many schools are actively developing bridge funding pools, extended payment plans, and emergency grants in response to the rule change. Your financial aid office knows which students are most exposed and can often unlock institutional aid that isn't publicly listed. Ask directly: "What solutions are you offering for students affected by the federal loan cap change?" They may have a designated NP-student support fund already underway.

Stay Flexible on Program Format

Part-time enrollment spreads costs across more semesters, reducing each term's borrowing need. Several online NP programs now offer per-credit tuition rates that keep annual costs within the $20,500 cap if you take a lighter course load. If your program allows it, shifting to part-time status for one year could buy time while the lawsuit progresses, without derailing your advancement.

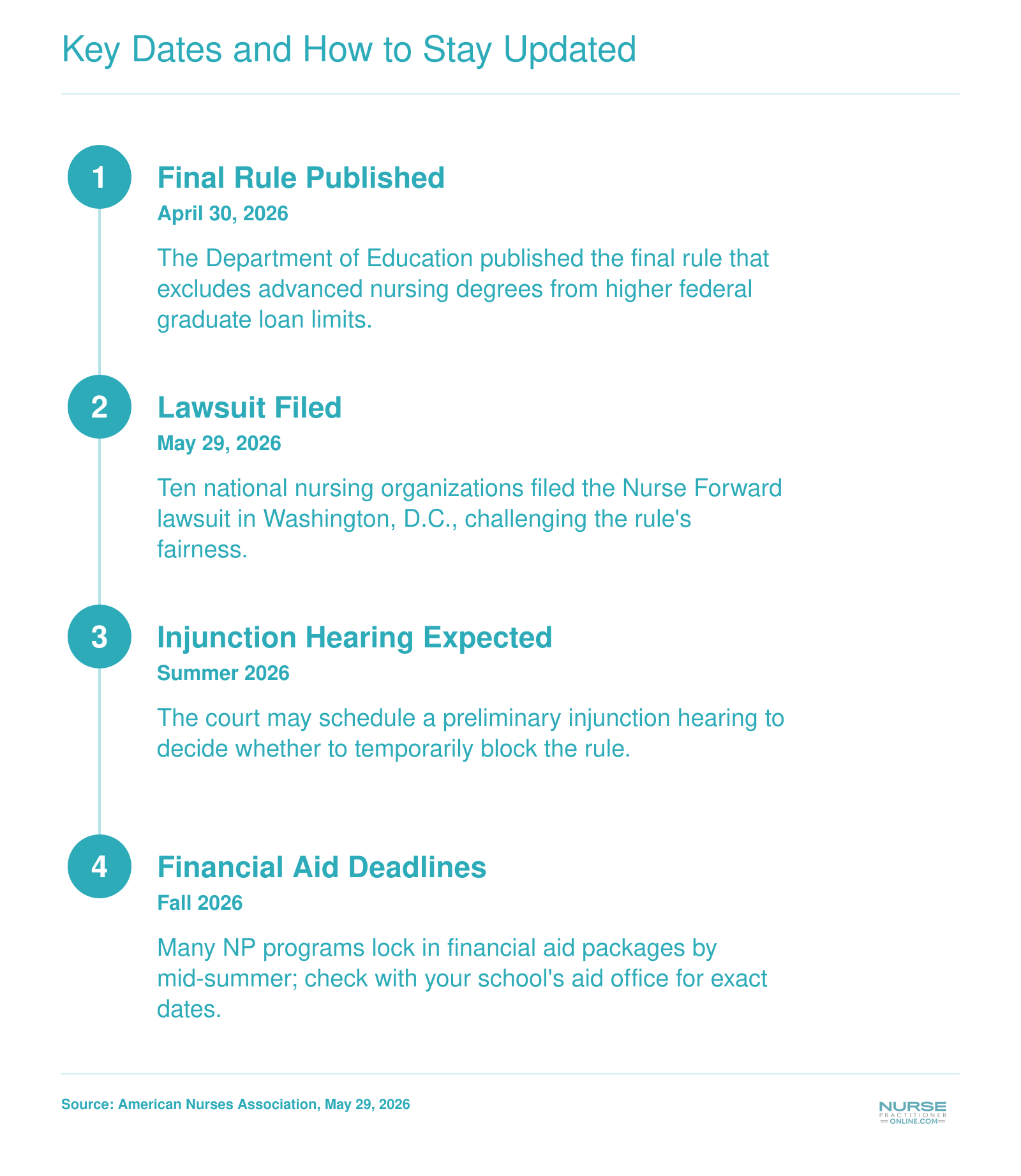

Key Dates and How to Stay Updated

Track the latest developments on the NP student loan lawsuit. Monitor the American Nurses Association (ANA) news page for official statements, follow the court docket via PACER, check the American Association of Colleges of Nursing (AACN) policy updates, and visit NursePractitionerOnline.com for ongoing analysis.

Frequently Asked Questions About the NP Student Loan Lawsuit

The Nurse Forward lawsuit raises urgent questions for current and prospective NP students about how federal loan caps may impact their education. Below are answers to the most common questions, based on the latest developments and what we’ve covered in this article.

- How will the new federal loan caps affect nurse practitioner students?

- Under the Department of Education’s rule, advanced nursing degrees are excluded from professional degree loan limits, capping NP students at lower graduate borrowing levels. This creates a potential funding gap between federal aid and the full cost of DNP, PhD, or MSN programs, forcing students to rely on private loans or out-of-pocket payments. The change adds significant financial strain to pursuing advanced practice education.

- What is the Department of Education's definition of a professional degree?

- For federal student aid, a professional degree typically includes programs like medicine, law, and pharmacy that prepare students for licensed practice. The final rule did not recognize post-baccalaureate nursing degrees as professional, despite arguments from nursing organizations that DNP and MSN programs meet the same criteria of readying graduates for advanced, licensed clinical roles.

- Which nursing organizations are suing the Department of Education?

- Ten organizations filed the lawsuit, including the American Nurses Association, American Association of Nurse Anesthesiology, Association of Women’s Health, Obstetric and Neonatal Nurses, American College of Nurse-Midwives, and Nurse Practitioners in Women’s Health. The coalition also includes specialty groups like the Academy of Neonatal Nursing and the Chi Eta Phi Sorority, representing a broad cross-section of advanced practice nursing.

- Will NP student loan limits change in 2026?

- The rule took effect in 2026, so NP students currently face the lower graduate loan caps. While the lawsuit filed in May 2026 seeks to overturn the exclusion, no immediate change occurs. If the court rules in favor of the nursing organizations, loan limits could be restored retroactively or prospectively, but students should plan for the current caps until a decision is reached.

- How do NP loan caps compare to PA and MD loan limits?

- Medical and PA programs are classified as professional degrees, allowing students to borrow up to the full cost of attendance. Under the new rule, NP students face lower annual and aggregate graduate loan caps. This disparity means a PA student can access substantially more federal aid than an NP student, despite similar educational investments and clinical practice scopes.

- What should NP students do to prepare for possible loan cap changes?

- Students should explore alternative funding such as HRSA scholarships, Nurse Corps loan repayment, or private loans. Contacting your program’s financial aid office to review all options is essential. Consider part-time enrollment to spread costs. Staying informed about the lawsuit’s progress is wise, but having a backup financial plan if the caps remain unchanged is the safest approach.

- Does this lawsuit affect PSLF eligibility or HRSA loan repayment programs?

- No, the lawsuit challenges only the borrowing limits, not loan forgiveness or repayment programs. NP students remain eligible for Public Service Loan Forgiveness and HRSA programs like the Nurse Corps, provided they meet the program requirements. The outcome of this case would only impact how much federal loan money students can access upfront, not existing forgiveness pathways.