Most important takeaways…

- A House bill reclassifying graduate nursing as a professional degree would double federal Stafford loan limits to $200,000.

- More than two dozen states sued the Education Department in 2026 over nursing's exclusion from professional degree status.

- Current loan caps of $138,500 already restrict many NP students, especially in expensive DNP and CRNA programs.

For years, advanced nursing programs have occupied an odd middle ground: academically demanding enough to rival law or medicine, yet excluded from the professional degree category that unlocks higher federal borrowing limits. The current $138,500 aggregate loan cap forces many NP students into private loans or part-time pacing. A June 2026 House Appropriations Committee amendment would change that by reclassifying graduate nursing as a professional degree, doubling the federal loan ceiling to $200,000.

The legislative move coincides with lawsuits from over two dozen states and nursing coalitions fighting for student loan forgiveness fighting the Education Department's narrower definition of professional study. Together, these actions could reshape how working nurses finance MSN, DNP, and CRNA programs. Even as the bill progresses, its package of cuts to other student aid programs highlights a persistent budget tension that will affect the entire nursing education pipeline.

What the House Bill and Lawsuits Mean for Graduate Nursing Students

A House appropriations bill could double the federal loan limits for graduate nursing students by reclassifying advanced nursing programs as professional degrees. This legislative push, combined with ongoing lawsuits, promises to rewrite the financial rules for MSN, DNP, and CRNA students.

The House Amendment: A Big Step Forward

On June 10, 2026, the House Appropriations Committee advanced an amendment designating graduate nursing programs as professional degrees within the fiscal year 2027 appropriations bill.1 If the full bill becomes law, nursing students pursuing advanced practice degrees would gain access to the higher federal borrowing limits reserved for professional programs: up to $50,000 per year and a $200,000 aggregate cap.2 That is a stark contrast to the current non-professional graduate limits of $20,500 annually and $100,000 aggregate,2 which have long constrained NP students who face tuition bills rivaling those of medical or dental programs.

Lawsuits Push Back on the Education Department's Exclusion

Earlier in 2026, the U.S. Department of Education released regulations that notably excluded graduate nursing from the list of eligible professional degree programs. This decision drew immediate pushback. In May 2026, a coalition of more than two dozen states filed one lawsuit, while a separate coalition of nursing organizations filed another, both challenging the exclusion.1 The following month, physician associate programs joined the fray with their own lawsuit, underscoring that this is a broad fight over how the government defines professional-level graduate education.

Where Things Stand Right Now (July 2026)

On June 25, 2026, a federal court granted a preliminary injunction in a case brought by eight trade associations, including the American Association of Nurse Practitioners and the Physician Assistant Education Association.2 The injunction blocks the Education Department's narrowed definition while the litigation proceeds. In response, the Department issued an interim expanded list of professional degree programs that now includes graduate nursing, effectively raising borrowing limits for NP students to professional-degree levels while the court order remains in effect.3 The House bill, meanwhile, has advanced out of committee but still needs approval from the full House, the Senate, and the president to become permanent law. For now, nursing students can access the higher loan caps, but the long-term outcome remains uncertain.

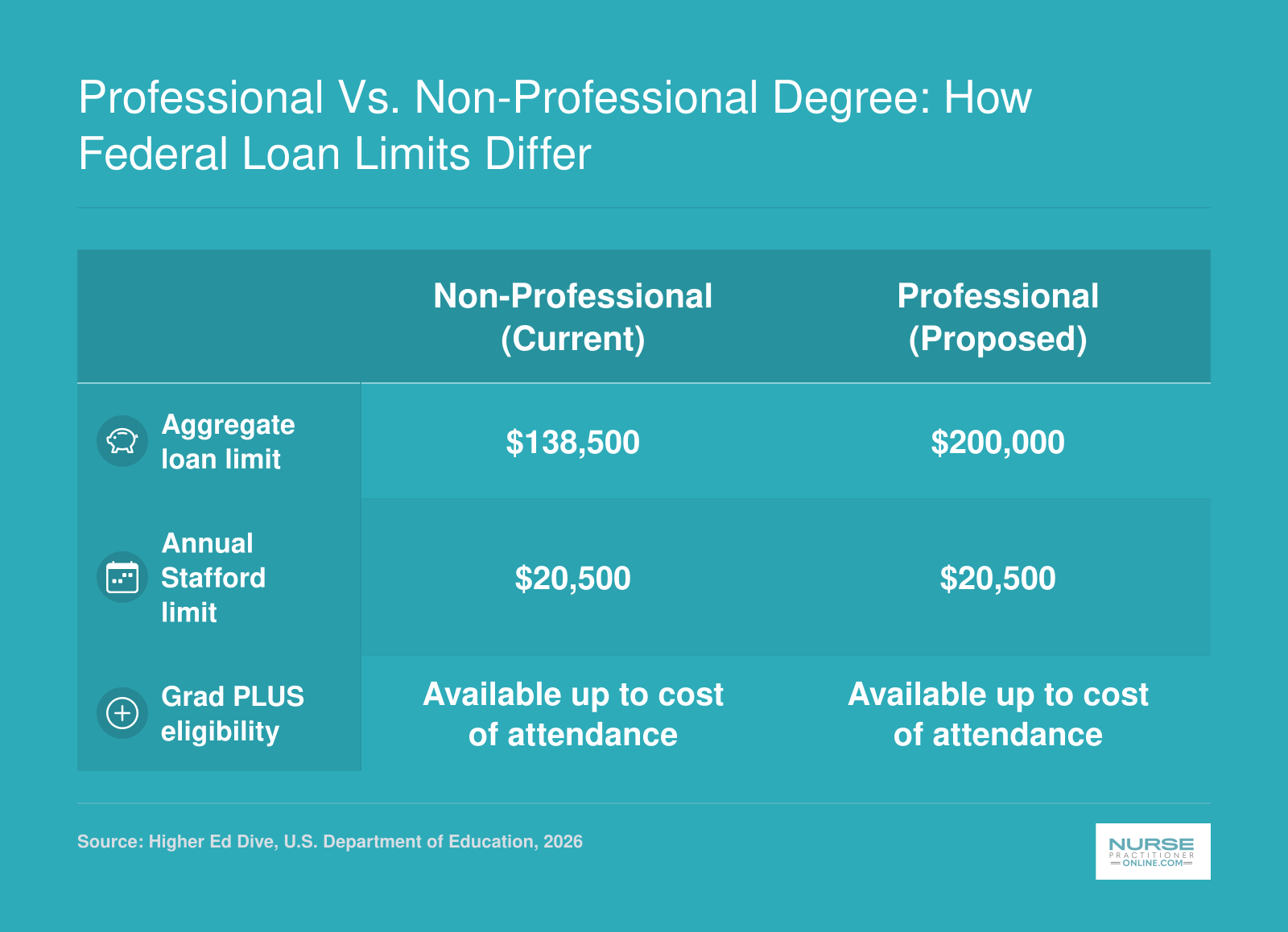

Professional Vs. Non-Professional Degree: How Federal Loan Limits Differ

The current federal loan system treats graduate nursing and other graduate programs the same, capping total Stafford loans at $138,500. Under the proposed professional degree designation, nursing students could borrow up to $200,000 in Stafford loans before turning to Grad PLUS, similar to medical or law students.

MSN Vs. DNP Vs. CRNA: Which Programs Are Most Affected

Graduate nursing programs vary widely in cost and duration, and the proposed loan cap increase would not affect all NP students equally. The current $138,500 aggregate federal loan limit already constrains many aspirants, but the financial strain falls hardest on those in the longest, most expensive tracks. Under the bill advancing through the House, designated professional nursing programs would allow borrowing up to $200,000, essentially doubling the limit for other graduate fields.

Where the Current Loan Cap Falls Short

Most graduate nursing students rely on federal Direct Unsubsidized Loans, which are capped at $138,500 including any undergraduate debt. For shorter MSN programs, that ceiling is often sufficient. Campus-based BSN-to-MSN programs typically run 2-3 years with total tuition ranging from $20,000 to $70,000. Online options keep costs on the lower end, leaving room for living expenses within the cap.

But the math changes for doctoral programs. DNP students, whether entering post-BSN or completing a post-master's degree, face 1.5-3 years of study and tuition between $20,000 and $60,000.2 While that range appears manageable, many DNP candidates already carry MSN debt that pushes their cumulative balance against the $138,500 ceiling. Understanding DNP program length by pathway can help students plan their borrowing timeline before they begin.

CRNA Programs Feel the Biggest Squeeze

The most acute pressure lands on CRNA programs. BSN-entry DNP or DNAP nurse anesthesia tracks last 3 years and frequently cost $60,000 to $180,000 in tuition alone.3 Factor in intensive clinical hours that preclude outside employment, and borrowing needs skyrocket. Even students with zero prior debt routinely exhaust the current $138,500 cap well before graduation. A bump to $200,000 would provide immediate breathing room and align federal loan limits more realistically with the true cost of CRNA education.

Post-master's CRNA completion degrees, often DNAP or DNP paths lasting 1.5-2 years with tuition of $25,000 to $50,000, are less affected simply because they build on existing credentials and often involve fewer credits. Yet these students, too, may have existing loans from their initial anesthesia training.

MSN Students: Less Pressure, But Not Immune

For traditional MSN tracks, the $138,500 limit rarely becomes a barrier unless a student carries significant undergraduate debt. A two-year online MSN may cost as little as $20,000, and even pricier options stay under $70,000. The professional degree designation matters most here for nurses who financed a prior bachelor's degree with loans and now need to layer graduate borrowing on top without hitting the aggregate limit. A higher cap offers a safety net, even for programs that look affordable on paper. Pairing a higher loan ceiling with nurse practitioner loan forgiveness programs could meaningfully reduce the long-term debt burden for NP graduates across all tracks.

Federal, Private, and Health-Professions Loans for NP Students

Understanding the differences between federal, private, and health-professions loans is essential for nurse practitioner students managing educational costs. Each option has unique rules for borrowing limits, interest charges, repayment terms, and forgiveness eligibility, which can significantly affect long-term financial health.

| Loan Type | Interest Rate | Annual/Aggregate Limits | Repayment Flexibility | Forgiveness Eligible |

|---|---|---|---|---|

| Federal Direct Unsubsidized Loan | Fixed rate set annually; e.g., 6.08% for 2025-2026 | Up to $20,500 per year; $138,500 aggregate (including undergrad) | Income-driven repayment (IDR) plans available; deferment and forbearance options for financial hardship, military, in-school | Eligible for Public Service Loan Forgiveness (PSLF) and IDR forgiveness after 20-25 years |

| Federal Grad PLUS Loan | Fixed rate, typically 1-2% higher than Direct Unsubsidized; e.g., 7.08% for 2025-2026 | Up to cost of attendance minus other financial aid; no aggregate limit | Same federal protections as Direct Unsubsidized: all IDR plans, generous deferment, and forbearance provisions | Eligible for PSLF and IDR-based forgiveness; may be consolidated with other federal loans for forgiveness |

| Private Student Loan | Variable or fixed, based on credit; rates can range widely (e.g., 4% to 15%) | Varies by lender; typically up to cost of attendance, less other aid; disclosure of aggregate caps is product-specific | Limited; often no IDR options; may offer brief forbearance or interest-only periods; in-school deferment common | Not eligible for federal loan forgiveness programs; some employers or state programs may offer assistance |

| HRSA Health Professions Student Loan (HPSL) | Fixed 5% interest rate throughout repayment | Based on financial need; annual and aggregate caps set by school; typically lower than federal limits | Deferment and forbearance available under specific conditions; no income-driven plans | May qualify for NHSC Loan Repayment Program or state-based primary care loan repayment programs |

Related Articles

How NP Salaries Support Loan Repayment

A high earning potential helps nurse practitioners manage their student loan obligations. The table below presents national salary percentiles for NPs based on the latest Bureau of Labor Statistics data.

| Salary Statistic | Annual Wage |

|---|---|

| Mean Annual Wage | $132,000 |

| Median Annual Wage | $129,210 |

| 25th Percentile | $109,940 |

| 75th Percentile | $149,570 |

Loan Forgiveness and Repayment Programs for Nurse Practitioners

As the legislative push to classify graduate nursing as a professional degree picks up steam, the menu of loan forgiveness and repayment programs for nurse practitioners remains robust. These options can dramatically lighten the debt load for NPs willing to work in underserved settings or commit to public service, making advanced practice financially viable even before any change to borrowing limits.

Public Service Loan Forgiveness for Nurse Practitioners

PSLF is one of the most accessible paths for NPs because a large share work in nonprofit hospitals, public health agencies, or VA medical centers, all qualifying employers. The program requires 120 qualifying monthly payments while employed full-time by a government entity or a 501(c)(3) nonprofit.1 Payments must be made under an income-driven repayment (IDR) plan, and after the 120th payment, the remaining loan balance is forgiven tax-free. The professional degree reclassification debate does not alter PSLF eligibility in any way; it only affects how much you can borrow in the first place. For an NP making consistent IDR payments over ten years in a qualifying job, the forgiveness can easily erase five or six figures of graduate debt.

Nurse Corps Loan Repayment Program

The Nurse Corps Loan Repayment Program targets NPs who commit to working in a Critical Shortage Facility. In exchange for a two-year service agreement, the program pays 60% of the nurse practitioner's total qualifying educational debt.2 A third year of service brings an additional 25%, covering up to 85% of outstanding loans.2 Eligible specialties include primary care, maternal health, and psychiatric mental health, and you must be an APRN or RN with an unencumbered license.2 The program also looks at financial need: your total qualifying educational loans must equal or exceed 100% of your annual salary.2 The FY 2026 application cycle closed on March 12, 2026,3 but the program runs annually, so NPs can prepare for the next window, typically opening early in the calendar year.4 With limited funding and high demand, submitting a complete application early is key.

State-Level Repayment Assistance

Beyond federal programs, many states operate their own loan repayment initiatives for nurse practitioners serving in underserved areas. These have varying eligibility rules, award amounts, and service obligations. For instance, a state may offer up to $50,000 in loan repayment for a two-year commitment in a rural clinic. Since programs are administered through state health departments or primary care offices, NPs should check their home state's website for current details. In some cases, you can stack a state award on top of Nurse Corps or PSLF, accelerating debt elimination.

Income-Driven Repayment Plans and NP Salaries

For NPs not on a direct forgiveness path, IDR plans, including SAVE, PAYE, IBR, and ICR, cap monthly payments at a percentage of discretionary income.1 Typical NP earnings in the $110,000 to $130,000 range lead to manageable payments, often between 10% and 15% of income after allowances for family size. Under SAVE, for example, a single NP earning $120,000 with $100,000 in graduate loans might pay around $600 per month. After 20 or 25 years of payments, any remaining balance is forgiven, though that forgiven amount may be taxable. IDR becomes especially powerful when paired with PSLF, as the 10-year clock resets after you've been making income-driven payments. Filing taxes separately from a spouse can further lower IDR payments, so working with a student loan counselor to model different scenarios is a smart step.

What the Broader Appropriations Bill Means for Nursing Students' Financial Aid

Subsidized Loans Disappear for Future BSN Students

Starting July 1, 2027, new federal Direct Subsidized Loans would no longer be issued to undergraduate students under this bill.1 For pre-licensure BSN students, that means every dollar borrowed for tuition and living expenses will begin accruing interest immediately, even while you're in school, during a grace period, or in deferment.2 Currently, subsidized loans help keep undergraduate debt manageable by covering interest until after graduation. Losing that benefit could add thousands of dollars in interest costs to a typical four-year nursing degree, especially for students who rely heavily on loans.

A Mixed Bag for Need-Based Aid

The bill does increase the maximum Pell Grant by $50, bringing it to $7,445 for the 2027-2028 academic year.1 However, it also slashes funding for two other vital programs: the Federal Supplemental Educational Opportunity Grant (FSEOG) is cut by 40%, and Federal Work-Study by 26%.2 These cuts could reduce the number of campus jobs and supplemental grants available to nursing undergraduates, hitting those from lower-income backgrounds hardest. While the bill dedicates roughly $16.27 billion in mandatory funding to address a Pell Grant shortfall,2 the trade-off is the elimination of subsidized loans: the savings from that program are used to shore up Pell.3

The Paradox for NP Aspirants

Here's the tension: the same sweeping appropriations bill that would double graduate nursing loan limits to $200,000 (if the professional degree designation sticks) simultaneously erodes the very financial aid infrastructure that helps nurses complete their BSN. For working nurses considering an NP path, this means that while advanced education may become easier to finance, the undergraduate pipeline could narrow. Fewer students may be able to afford nursing school without taking on high-interest debt, potentially affecting the future NP workforce. NP student loan forgiveness programs may help offset some of that burden, but legislative wins in one area can still come with offsets that reshape the broader educational landscape.

What Happens Next: Timeline and How to Prepare

The path to higher loan limits for NP students is unfolding through legislation and litigation. Here are answers to common questions, along with steps you can take now to protect your financial aid strategy.

- What happens to current NP students' loans if nursing loses professional degree status?

- If nursing loses professional designation, current NP students would revert to standard graduate loan limits of about $20,500 annually in Direct Unsubsidized Loans. Total aggregate limit would drop to $138,500, far below DNP costs. Students already borrowing at the higher $200,000 cap might not be affected retroactively. To prepare, explore health professions loans and private or employer-sponsored options to bridge potential gaps.

- Can nurse practitioners qualify for Public Service Loan Forgiveness?

- Yes, nurse practitioners often qualify for Public Service Loan Forgiveness (PSLF) if they work full-time for a qualifying nonprofit or government employer and make 120 eligible payments under an income-driven repayment plan. Many NP roles in hospitals, community clinics, and public health meet the criteria. Submit an Employment Certification Form annually and consider consolidating loans into a Direct Loan to stay on track.

- Do DNP and MSN students have different federal loan limits right now?

- Currently, both DNP and MSN programs are categorized as graduate, not professional, degrees. So both face the same loan caps: $20,500 in Direct Unsubsidized Loans per year, with an aggregate limit of $138,500. CRNA programs sometimes have higher borrowing through health professions loans. If the bill passes, all graduate nursing programs would get the $200,000 professional limit, equalizing DNP and MSN borrowing.

- When will the professional degree designation take effect if the bill passes?

- If the House and Senate pass the FY2027 appropriations bill with the amendment, and the president signs it, the change would likely become effective for loan periods beginning on or after July 1, 2027. The Department of Education would need to update regulations. In the meantime, the lawsuits could force an earlier change if courts rule against the department's exclusion.

- What should prospective NP students do right now to prepare financially?

- First, maximize federal unsubsidized loans. Then explore health professions loans, scholarships, and assistantships. Compare total program costs and projected salary. Consider signing up for an income-driven repayment plan and look into employer tuition assistance. Track the bill's progress and any court rulings. If possible, defer enrollment until the loan limit increase is official to reduce private borrowing.

- Does the judge's ruling apply to all graduate nursing programs or only certain degree types?

- As of July 2026, no judge has issued a final ruling. The lawsuits filed by states and nursing associations challenge the Education Department's exclusion of all graduate nursing programs from the professional degree list. A potential court decision could mandate including all master's and doctoral nursing programs, not just select tracks. Follow developments closely, as a ruling could come before the bill's passage.