Most important takeaways…

- NP students at public universities typically spend $35,000 to $55,000 total, while private programs can cost over $100,000.

- Stacking NHSC loan repayment with Public Service Loan Forgiveness at a qualifying health center can eliminate six figures of debt.

- Grad PLUS loans are no longer available to new graduate borrowers as of July 1, 2026, reshaping how NP students finance their degrees.

- Employer tuition reimbursement at most hospitals caps at $5,250 per year, matching the federal tax-free threshold.

Nurse practitioner students graduate with anywhere from $40,000 to well over $100,000 in education debt, a spread wide enough that two nurses in the same MSN cohort can leave school with very different financial futures. The gap rarely comes down to income. It comes down to which funding levers a student pulled, and when.

The stress is real. Prospective NP students routinely describe losing sleep over whether the degree will pay off, especially when a partner's income shifts or a household hits an unexpected expense mid-program. That anxiety is warranted, but it is also solvable.

Scholarships, employer tuition benefits, federal loans, nurse practitioner loan forgiveness programs, and program-selection choices each move the number down independently. Stack two or three of them, and the debt load at graduation often looks nothing like the sticker price that scared you off in the first place.

How Much Does NP School Actually Cost?

The sticker price you see on a nurse practitioner program website tells only part of the story. Most schools advertise tuition per credit hour or per semester, but the true cost of earning your NP degree includes dozens of expenses that add up quickly: textbooks and clinical software subscriptions, preceptor placement fees (sometimes $500 to $2,000 per clinical rotation), malpractice insurance, travel to clinical sites, background checks, drug screens, immunization updates, and certification exam fees. When you factor in lost income if you reduce your nursing shifts and everyday living expenses over two to four years, the real number can double or triple the advertised tuition.

Tuition Ranges by Program Type

Online MSN programs typically cost between $25,000 and $77,000 for the entire degree1, while online DNP programs range from $44,000 to $172,000. The wide spread reflects the difference between public in-state tuition and private universities. Public DNP programs average about $561 per credit hour, compared to $1,024 per credit at private institutions. For context, Duke University charges $2,250 per credit for graduate nursing during the 2025-2026 academic year3, while the University of Texas at Austin offers a DNP for approximately $30,000 total.4 Understanding MSN vs DNP differences in scope and credit requirements helps explain why costs vary so dramatically between program types.

Post-Master's DNP programs (for nurses who already hold an MSN) cost less overall because they require fewer credits. Public in-state post-MSN DNP programs generally run between $21,318 and $38,912, while private post-MSN programs cluster around $38,912. BSN-to-DNP programs, which combine the Master's and doctoral levels, total roughly $40,953 to $74,752.

Hidden Fees and Real Total Cost

Online programs often advertise lower per-credit rates but tack on technology fees, clinical coordination charges, and virtual lab access fees that inflate the final bill. Most affordable nurse practitioner programs are public in-state options, which remain the most budget-friendly path overall when you account for all mandatory expenses. A realistic total budget includes not just tuition but also $3,000 to $5,000 for books and supplies, $1,000 to $3,000 in clinical placement and compliance costs, and your ongoing rent, food, insurance, and transportation.

Average Graduate Debt at Completion

Nurse practitioner students who borrow to finance their degrees graduate with an average debt load that varies widely by program type and personal circumstances. Many working nurses report carrying $40,000 to $80,000 in combined undergraduate and graduate loans by the time they earn their NP credentials, though those who attend expensive private programs or pursue a DNP without employer assistance can finish with six-figure balances.5 Understanding the real cost upfront helps you make smarter financing decisions before you commit to a program.

NP School Cost Breakdown: Where Your Money Goes

Understanding where your money goes can help you plan smarter. For a typical two-year MSN program at a public university, total costs generally fall between $35,000 and $55,000. Tuition is by far the largest expense, but clinical placement fees, campus fees, and everyday living costs add up faster than most students expect.

Scholarships and Grants for NP Students

Free money exists for NP students, and most of it goes unclaimed each cycle because nurses assume they won't qualify or run out of time to apply. If you commit even a few weekends to scholarship applications, you can meaningfully reduce what you borrow, and in some cases eliminate tuition entirely in exchange for a service commitment.

Federal Service-Based Scholarships

The National Health Service Corps (NHSC) Scholarship is the heaviest hitter for primary care NP students. It covers tuition, required fees, other educational costs, and a monthly living stipend for up to four years of full-time study.1 In exchange, you commit to two to four years of full-time clinical practice at an NHSC-approved site in a Health Professional Shortage Area (HPSA) after graduation.2 To qualify for 2026, you must be a U.S. citizen or national, enrolled full-time at an accredited program, and pursuing a primary care track: family, adult-gerontology, pediatric, psychiatric-mental health, or women's health NP.3 Applications for the 2026 cycle close April 16, 2026, and awardees must start school on or before September 30, 2026.2

The Nurse Corps Scholarship Program is a close cousin but with important differences. It is open to U.S. citizens, nationals, and lawful permanent residents; it accepts a broader range of nursing degree programs including NP tracks; and it prioritizes applicants with the greatest financial need.4 The service commitment is also two to four years, but placements can include Critical Shortage Facilities such as hospitals and public health clinics, not just NHSC primary care sites. If loan repayment fits your timeline better than upfront scholarship, the nurse practitioner loan repayment programs like the NHSC Loan Repayment Program offer up to $50,000 for a two-year commitment after you're already licensed and practicing.1

Private and Professional Scholarships

Stack smaller awards from professional organizations to fill the gaps:

- AANP Foundation Scholarships: Typically $2,500 to $5,000 for AANP student members enrolled in an accredited NP program.

- ONS Foundation: Awards for NP students pursuing oncology specialization, generally in the $3,000 to $5,000 range.

- National Black Nurses Association (NBNA): Multiple named scholarships ranging from roughly $1,000 to $6,000 for NBNA student members.

- State nursing associations: Nearly every state affiliate offers scholarships, often less competitive than national awards. Amounts vary from $500 to $5,000.

Three Rules That Actually Work

Apply early: many awards use rolling review, and late applications get thinner attention. Tailor every essay to mission alignment, particularly around underserved and rural care, since selection committees are looking for candidates who match their organization's purpose, not generic strong students. Stack five to ten smaller awards rather than pinning hopes on one large scholarship. A $2,000 award you actually win beats a $20,000 award you don't. Joining a nurse practitioner organization with scholarship programs, like AANP, is one of the fastest ways to access members-only funding.

One tax note: scholarship dollars applied to tuition, required fees, and books are tax-free. Any portion covering living stipends, room, or board is taxable income and should be reported. Keep receipts and talk to a tax preparer familiar with health professions education before filing.

Questions to Ask Yourself

Employer Tuition Reimbursement for NP Students

HCA Healthcare, the largest for-profit hospital operator in the U.S., caps its education assistance benefit at $5,250 per calendar year1, an amount that lines up precisely with the federal tax-free threshold most employers use as their benchmark. If you work in a hospital or health system, this benefit is often the single biggest lever you can pull to lower your out-of-pocket cost for NP school.

How Hospital Reimbursement Programs Typically Work

Most health-system tuition programs share a similar structure: you enroll in an accredited program, maintain a minimum GPA (usually B or better), submit grades and receipts after each term, and get reimbursed up to an annual cap. Benefits generally run from $3,000 to over $10,000 per year, with the exact figure depending on your role, employment status, and years of service.

A few reference points among large employers:

- HCA Healthcare: Up to $5,250 per calendar year2, available to full-time and part-time colleagues after 90 days of service3, with no post-graduation service commitment. PRN staff are generally excluded or fall under different rules. HCA also offers a 5% tuition discount and direct billing at Galen College of Nursing.1

- Kaiser Permanente, VA facilities, and large academic medical centers: Often offer benefits in a similar $5,000 to $10,000+ range, though details vary widely by union contract, region, and role. Some VA programs and academic centers layer additional NP-specific scholarships on top of general tuition assistance.

Service commitments are more common at systems that offer larger up-front amounts or full-ride sponsorships. A typical commitment is one to two years of post-degree employment, with prorated repayment if you leave early.

The IRS Section 127 Rule You Need to Know

Under IRS Section 127, the first $5,250 per year of employer-provided educational assistance is excluded from your taxable income. Anything above that threshold is generally treated as taxable wages, which means a $10,000 benefit can effectively shrink once federal, state, and payroll taxes are applied. Factor that into any offer that looks unusually generous. If you plan to combine reimbursement with borrowing, it is worth reviewing nurse practitioner loan forgiveness programs so you understand how employer benefits interact with federal repayment options.

How to Negotiate and Confirm the Benefit

Ask before you enroll, not after. Once you have a written policy in hand, verify four things: whether graduate NP programs are pre-approved or require case-by-case approval, whether part-time students qualify, whether clinical hours or certification exam fees are covered, and whether any service commitment is triggered. Get every commitment in writing from HR, not just from your manager. If your employer pre-approves specific schools, that list can also steer you toward more affordable programs you had not considered.

Federal and Private Loan Options Compared

The rules for borrowing money to pay for nurse practitioner school changed significantly on July 1, 2026, and the biggest shift is the elimination of Grad PLUS loans for new graduate borrowers.1 Until this summer, NP students could borrow up to the full cost of attendance using a combination of Direct Unsubsidized Loans and Grad PLUS loans. That safety net is gone for students entering programs after the cutoff, which makes understanding the new federal loan caps and when to consider private loans more important than ever.

The End of Grad PLUS and the New Borrowing Caps

Effective July 1, 2026, the U.S. Department of Education stopped offering new Grad PLUS loans to graduate and professional students.1 In its place, graduate borrowers now face stricter annual and aggregate limits on federal Direct Unsubsidized Loans.2 For most NP students, who are classified as graduate students, the maximum annual unsubsidized loan is $20,500, with an aggregate limit of $100,000.3 Students in programs classified as professional (a smaller subset) may be eligible for up to $50,000 per year and a $200,000 aggregate cap.3 All federal student loan borrowers share a lifetime limit of $257,500.4

There is one exception: if you received at least one Direct Loan disbursement for the same graduate program before July 1, 2026, you may retain Grad PLUS eligibility for up to three additional academic years, or until you complete the program.5 For everyone else starting NP school this year or later, the Grad PLUS option is off the table.

How the New Limits Affect NP Students

Before July 2026, a student in a high-cost NP program could count on Grad PLUS to cover any tuition and living expenses that exceeded the base federal loan limit. Now, a graduate-level NP student who needs, say, $40,000 per year in tuition and fees will face a significant funding gap: the $20,500 annual cap may only cover half of that.6 This makes the total price tag of a program more critical than ever. An online MSN NP program that is affordable suddenly looks even more attractive compared to an expensive private school.

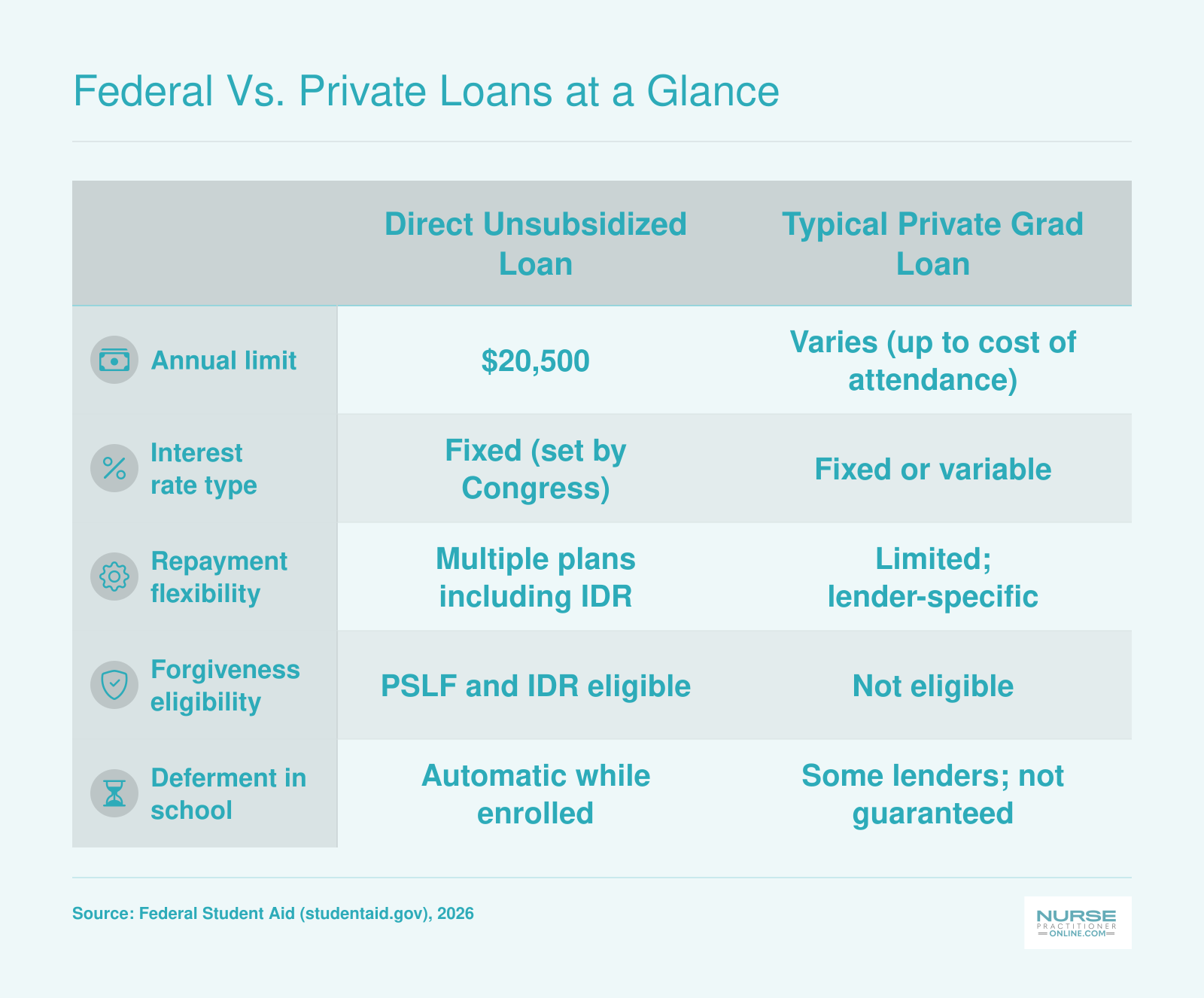

Federal vs. Private Loans: A Clear Comparison

When federal loans fall short, private loans from banks, credit unions, or online lenders can fill the gap. But the two options are not interchangeable.

- Federal Direct Unsubsidized Loans: Fixed interest rates set by the government each academic year, no credit check required, and automatic access to income-driven repayment plans (like IDR) and nurse practitioner loan forgiveness programs (PSLF, NHSC). Interest accrues while you are in school, but deferment and forbearance options are generous.

- Private student loans: Interest rates depend on your credit score and can be fixed or variable. They are not eligible for any federal forgiveness program or income-driven repayment. Deferment or forbearance during financial hardship is typically more limited and less flexible.

Because federal loans carry irreplaceable protections, always max out your eligibility for Direct Unsubsidized Loans first. Only after exhausting that $20,500 (or $50,000) each year should you consider a private loan for any remaining balance.

What to Do If You Face a Funding Gap

If the new caps create a shortfall for your NP program, do not rush into the first private loan offer you find. Request rate quotes from at least three lenders and compare the annual percentage rate (APR), repayment term, any origination fees, and the forbearance policy. Look for lenders that offer a grace period after graduation and income-based repayment options, even if those are less flexible than the federal versions. The loss of Grad PLUS means program cost has moved from a secondary concern to a primary factor in your school selection: choosing wisely on the front end is the single most powerful way to avoid crushing debt later.

Federal Vs. Private Loans at a Glance

When scholarships and employer aid don't cover the full bill, loans fill the gap. The two main categories work very differently, so understanding the trade-offs before you borrow is essential.

Loan Forgiveness and Repayment Programs for NPs

Even after exhausting scholarships, grants, and employer tuition assistance, many NP students still graduate with substantial loan balances. The good news: several federal and state programs can eliminate a significant portion of your debt in exchange for service in high-need settings. Understanding which programs you might qualify for can shape both your borrowing decisions and your early career choices.

Major Loan Forgiveness Programs Compared

Here is a side-by-side look at the primary federal and state options available to nurse practitioners in 2026:

- NHSC Loan Repayment (Standard): Up to $75,000 for a two-year commitment at an NHSC-approved site in a Health Professional Shortage Area.1 You must be a U.S. citizen or national, hold an active NP license, and participate in Medicare, Medicaid, or CHIP.2

- NHSC Rural Community Loan Repayment: Up to $100,000 for three years of service in rural HPSAs or rural substance use disorder treatment settings. Requirements mirror the standard program but target rural communities specifically.

- NHSC SUD Workforce Loan Repayment: Up to $75,000 for three years at approved outpatient substance use disorder treatment sites. NPs with medication-assisted treatment certification are eligible.4

- Nurse Corps Loan Repayment: Covers 60 percent of qualifying nursing education debt for a two-year commitment at a Critical Shortage Facility or as nursing faculty. An optional third year adds another 25 percent of your original balance.5

- Indian Health Service Loan Repayment: Up to $40,000 for two years at IHS, tribal, or urban Indian health facilities serving American Indian and Alaska Native communities.6

- State Loan Repayment Programs (SLRP): Awards vary by state but can reach $50,000 or more for two years of service. Each state designs its own program, though many require placement at NHSC-approved sites and receive federal matching funds.6

Public Service Loan Forgiveness Explained

PSLF remains one of the most powerful options for NPs, yet many qualifying nurses do not realize they are eligible. The program discharges your entire remaining federal Direct Loan balance after you make 120 qualifying monthly payments while working full-time for a qualifying employer. That works out to roughly ten years of service.5

Qualifying employers include federal, state, local, and tribal government agencies, as well as 501(c)(3) nonprofit organizations. This means NPs working at nonprofit hospitals, federally qualified health centers, community health centers, and many academic medical centers likely qualify without any special application to a shortage area. For a deeper look at how these programs stack up, nurse practitioner loan forgiveness programs are covered in detail in our dedicated guide.

To qualify, your loans must be federal Direct Loans, and you must be enrolled in an income-driven repayment plan such as SAVE, PAYE, or IBR. Payments made under the standard ten-year plan also count, though most borrowers benefit from IDR plans that keep monthly payments lower while they work toward forgiveness.

Tax Treatment of Forgiven Debt

Understanding how forgiven debt is taxed can prevent an unpleasant surprise years down the road. PSLF forgiveness is permanently tax-free at the federal level. You will not owe income tax on the discharged balance.

Forgiveness under income-driven repayment plans after 20 or 25 years is a different matter. This type of forgiveness was temporarily made tax-free through 2025 under pandemic-era legislation. For balances forgiven after 2025, the tax treatment is uncertain and may revert to being counted as taxable income. If you anticipate IDR forgiveness rather than PSLF, verify the current rules with a tax professional or the Department of Education before making long-term plans.

Combining Programs Strategically

Some NPs layer multiple programs. For example, you might accept an NHSC award during your first two to three years, making your PSLF qualifying payments simultaneously. When the NHSC service ends, you continue in a qualifying public service role until you hit 120 payments. This approach can maximize total debt reduction while building clinical experience in underserved communities that often offer meaningful work and strong mentorship.

Budgeting and Working While in NP School

The tension between maintaining an income and completing a rigorous graduate program defines the financial reality for most NP students today. The good news: yes, many nurses successfully work while earning their NP degree. The challenge lies in understanding exactly when that is feasible and planning your finances around the semesters when it is not.

Can You Really Work While in NP School?

The answer depends almost entirely on your program format and where you are in the curriculum. Part-time and online programs are specifically designed for working nurses, with asynchronous coursework and evening or weekend schedules that accommodate shift work. During didactic semesters, many students maintain 24 to 36 hours per week at their nursing jobs without sacrificing academic performance.

Clinical rotations change the equation dramatically. Most NP programs require between 500 and 1,000 or more clinical hours, and these rotations typically occur during standard business hours when preceptors are available. During clinical semesters, full-time work becomes nearly impossible for most students. Some manage to pick up one or two weekend shifts, but attempting to work your usual schedule while completing 20 or more clinical hours per week is a recipe for burnout and academic trouble. How hard is NP school is a question worth researching before you commit to a work schedule, because clinical intensity varies considerably by specialty and program.

Practical Strategies to Reduce Costs

Smart planning can significantly reduce what you need to borrow:

- Negotiate flexible scheduling: Talk to your manager before starting your program. Many employers will accommodate per-diem or weekend-only schedules during didactic semesters, preserving your income when coursework allows.

- Maximize employer tuition benefits: If your hospital offers tuition reimbursement (often $3,000 to $5,250 annually), structure your enrollment to capture the maximum benefit each calendar year.

- Claim the Lifetime Learning Credit: This federal tax credit provides up to $2,000 per year for qualified education expenses. It is available even if you are not pursuing a degree for the first time.

- Secure local preceptors early: Clinical site placement can require significant travel if you end up at a distant location. Networking with local providers and using your employer's connections can save hundreds in gas and lodging costs each semester.

Building a Realistic Budget

Before borrowing, calculate exactly what you need beyond scholarships and savings. A realistic monthly budget for an NP student might look something like this:

- Rent or mortgage: $1,200 to $1,800

- Food and household expenses: $400 to $600

- Health insurance: $150 to $400

- Transportation (car payment, gas, insurance): $350 to $550

- Loan interest (if accruing during school): $50 to $150

- Miscellaneous and emergency fund: $150 to $250

Total your expected expenses for the full program duration, then subtract your projected income during each semester (remembering that clinical semesters will likely mean reduced hours). The gap between expenses and income, minus any scholarships or grants, represents your true borrowing need. Many students discover they can reduce their loan total by 20 to 30 percent simply by planning ahead rather than borrowing the maximum offered amount. Avoiding common MSN NP program enrollment mistakes at the start can also prevent costly mid-program corrections.

The Emotional Reality of Financial Stress

Financial pressure during NP school is not just a spreadsheet problem. It compounds academic stress, strains relationships, and can make you question whether you made the right decision. These feelings are normal and widely shared among NP students. The antidote is preparation: knowing your numbers, having a plan for lean semesters, and building a small emergency cushion before clinical rotations begin. Students who enter their program with a clear financial roadmap report feeling more confident and less anxious, even when unexpected expenses arise.

Choosing an Affordable NP Program

The program you pick matters more than any scholarship you win. Tuition sticker price varies by a factor of five or more across NP programs, and the differences compound with fees, clinical costs, and time-to-completion.

Compare Program Types Honestly

Online public programs at in-state rates are typically the most affordable path to NP licensure. Expect total tuition in the $15,000 to $40,000 range at a public university where you qualify for in-state rates, versus $60,000 to $120,000 or more at private universities and name-brand online programs. On-campus programs add commuting, parking, and often lost income from inflexible clinical schedules.

MSN versus DNP is the other big lever. An MSN gets you to NP practice in roughly 2 to 3 years; a BSN-to-DNP adds a year or more of tuition and living expenses. Unless your specialty or long-term goal requires the doctorate, the MSN is the cheaper on-ramp, and you can bridge to DNP later after a few years, often with employer support.

Part-Time vs. Full-Time Enrollment

Part-time enrollment stretches the degree over 3 to 4 years, but it lets you keep working full-time and tap employer tuition reimbursement year after year. If your employer caps reimbursement at $5,250 annually (the tax-free federal limit), stretching a 3-year program to 4 years means one extra year of that benefit, plus continued salary and retirement contributions. For many nurses, part-time enrollment cuts out-of-pocket costs by half or more.

Ask About Hidden Program Aid

Standard financial aid packages rarely tell the full story. Ask the program director directly about:

- Graduate assistantships or teaching assistant positions that waive tuition

- Clinical fellowships tied to partner health systems

- Tuition discounts for preceptors or nurses employed by affiliated hospitals

- Scholarships restricted to enrolled students that aren't advertised publicly

Don't Chase the Lowest Sticker Price

A program that saves you $5,000 in tuition but has a 60% AANP pass rate or leaves you scrambling to find your own clinical placements will cost far more in delayed income and retake fees. Before enrolling, review common mistakes to avoid when enrolling in an MSN NP program, then verify graduation rates, board pass rates for AANP or ANCC, and whether the program places students in clinical sites or expects you to find your own. Long-term ROI beats short-term savings every time.

Related Articles

Tax Breaks and Hidden Savings for NP Students

Federal tax law offers several overlooked breaks that can reduce the actual cost of your NP degree by thousands of dollars each year. The trick is knowing which benefits apply to your situation and how to claim them correctly when April arrives.

Tax-Free Employer Tuition Reimbursement

If your hospital or clinic pays part of your tuition, the first $5,250 per year is completely tax-free under IRS Section 127.1 This exclusion covers tuition, fees, books, supplies, equipment, and even student loan payments your employer makes on your behalf.1 The $5,250 cap is per employee per calendar year through 2026, and starting in 2027 the limit will adjust for cost-of-living increases.2

One catch: you cannot use expenses that were paid tax-free by your employer to also claim the Lifetime Learning Credit. The IRS does not allow double-dipping.3

Lifetime Learning Credit for Graduate Students

Graduate students enrolled in NP programs can claim up to $2,000 per year through the Lifetime Learning Credit.3 This credit applies to tuition and required fees you pay out of pocket (or with loans). You cannot claim the credit for expenses covered by tax-free scholarships or the Section 127 exclusion, so plan which dollars to apply where.3

When Scholarship Money Is Taxable

Most NP students assume all scholarship funds are tax-free. They are only if the money pays for tuition, required fees, books, supplies, and required equipment.3 Any portion used for living expenses, stipends, travel, or optional gear counts as taxable income and must be reported on your return.3 If you receive a $10,000 scholarship and $3,000 goes toward rent, you owe tax on that $3,000.

Student Loan Interest Deduction

Once you graduate and begin repayment, you can deduct up to $2,500 per year in student loan interest. This deduction phases out at higher income levels, but most new NPs qualify during their first few years in practice.

Tax Treatment of Loan Forgiveness

Public Service Loan Forgiveness remains permanently tax-free. NHSC and Nurse Corps awards are also excluded from taxable income. However, if you plan to pursue income-driven repayment forgiveness after 20 or 25 years, the tax treatment depends on whether Congress extends the temporary tax-free provision that expired at the end of 2025. As of mid-2026, forgiveness under IDR plans may be taxable again unless new legislation passes. Review the details of nurse practitioner loan forgiveness programs before you assume forgiven balances are tax-free.

Is NP School Worth It Financially?

The central question comes down to whether the salary increase justifies the upfront investment, and for most nurses, the math works out clearly in favor of advancing to the NP role.

The Earnings Differential

Median registered nurse salaries hover around $86,000 annually, while nurse practitioners earn a median of approximately $126,000. That roughly $40,000 yearly increase represents the core of your return on investment. Even if you graduate with $80,000 to $100,000 in student debt, the earnings gap alone can help you recoup that investment within three to five years of starting your NP career. After that point, every additional year of practice means that $40,000 difference flows directly to your financial goals rather than debt repayment. Your earning potential can also vary significantly depending on specialty, so it is worth exploring highest paid nurse practitioner specialties as you plan your path.

Three Repayment Scenarios

Consider how different approaches play out for someone with $80,000 in federal loans at 7 percent interest:

- Aggressive payoff: Devoting $2,000 monthly toward loans on your NP salary eliminates the debt in roughly four years with about $12,000 in total interest. You sacrifice short-term spending flexibility but emerge debt-free relatively quickly.

- Standard 10-year repayment: Monthly payments around $930 result in approximately $31,000 in total interest paid. This approach balances manageable payments with a defined payoff timeline.

- PSLF track: Working for a qualifying nonprofit or government employer while making income-driven payments for ten years leads to forgiveness of any remaining balance. Monthly payments stay lower early in your career, and if you remain in public service, you avoid paying the full loan amount plus interest.

Each path has tradeoffs, but none leaves you in an unmanageable financial position given NP earning potential. For a deeper look at how each forgiveness program works, the nurse practitioner loan forgiveness guide walks through eligibility and timelines in detail.

Debt-to-Income Perspective

Even at the high end of NP educational debt, your debt-to-income ratio remains far more favorable than what graduates carry in many other fields. Financial planners and lenders generally view NP debt as manageable because your earning power supports reasonable repayment timelines. A $100,000 debt load on a $126,000 salary represents less than one year of gross income, which compares favorably to law school or MBA graduates who often carry similar or higher debt with less predictable job markets.

Beyond the Numbers

Financial calculations matter, but they do not capture everything. Many nurses pursue NP credentials for greater autonomy, expanded scope of practice, and deeper career satisfaction. These nonfinancial benefits are harder to quantify but often prove just as valuable as the salary increase. That said, when the question is purely financial, the data supports a clear conclusion: NP school represents a sound investment that most working nurses can afford and repay without sacrificing their financial futures.

Frequently Asked Questions About Paying for NP School

Paying for an NP degree raises a lot of practical questions, especially when you are juggling work, family, and existing student loans. Below are straightforward answers to the financing questions we hear most often from working nurses considering NP programs.

- Can I get NP school paid for entirely through employer tuition reimbursement?

- It is possible but uncommon. Most employers cap annual tuition reimbursement between $5,000 and $10,000, while full NP program costs typically range from $30,000 to over $100,000. Some large health systems and the military offer more generous benefits that can cover the full cost, but they usually require a multi-year service commitment afterward. Stacking reimbursement with scholarships and grants is a more realistic path to graduating debt free.

- What is the NHSC scholarship and how do I apply as an NP student?

- The National Health Service Corps (NHSC) scholarship covers tuition, fees, and a monthly living stipend for NP students who commit to practicing in a federally designated Health Professional Shortage Area after graduation. The service obligation is typically two to four years. Applications open each spring through the NHSC website. You must be enrolled or accepted into an accredited NP program and be a U.S. citizen or national. Competition is strong, so apply early and tailor your personal statement to primary care in underserved communities.

- How much debt do NP students typically graduate with?

- Debt levels vary widely depending on program type and whether you attend a public or private institution. Many NP graduates report carrying between $40,000 and $80,000 in student loan debt, though students at private universities sometimes exceed $100,000. Working nurses who use employer reimbursement, scholarships, or attend affordable public programs can graduate with significantly less. Tracking your total borrowing semester by semester helps prevent surprises at graduation.

- Can I work full time while attending NP school?

- Many online and hybrid NP programs are designed for working nurses, and a large share of students do maintain full-time employment, at least during the didactic portion. Clinical rotations are harder to combine with a 36-hour-plus work schedule because preceptor hours are often during weekdays. Talk to your employer early about schedule flexibility, and consider reducing to part time during clinical semesters. Maintaining income while in school is one of the most effective ways to reduce borrowing.

- What changed with federal graduate student loans in July 2026?

- As of July 2026, changes to federal graduate lending are still evolving. Grad PLUS loan interest rates reset each July based on the 10-year Treasury note, so your rate depends on when you borrow. Recent legislative proposals have targeted borrowing limits and income-driven repayment plan terms, but final rules can shift. Check the Federal Student Aid website for the most current rates and repayment options before you accept any loan package, and compare them against private lender offers.

- Are there special funding options for nontraditional or second-degree NP students?

- Yes. Several scholarship programs specifically target career changers, second-degree students, and nurses from underrepresented backgrounds. The HRSA Nursing Workforce Diversity grants, AACN minority scholarships, and many state nursing associations offer awards for nontraditional applicants. Direct-entry or accelerated BSN-to-DNP students may also qualify for the same federal loan and NHSC programs as traditional NP students. Check with your program's financial aid office, because eligibility rules for institutional scholarships vary.