Most important takeaways…

- PSLF, NHSC, NURSE Corps, and state programs can each eliminate tens of thousands of dollars in NP student debt.

- NPs can combine programs by running them sequentially, though applying the same loan dollar to two programs simultaneously is not allowed.

- PSLF forgiveness remains tax free at the federal level, but some other forgiven amounts became taxable again in 2026.

- Submitting the PSLF Employer Certification Form now, even before you finish school, protects your qualifying payment count.

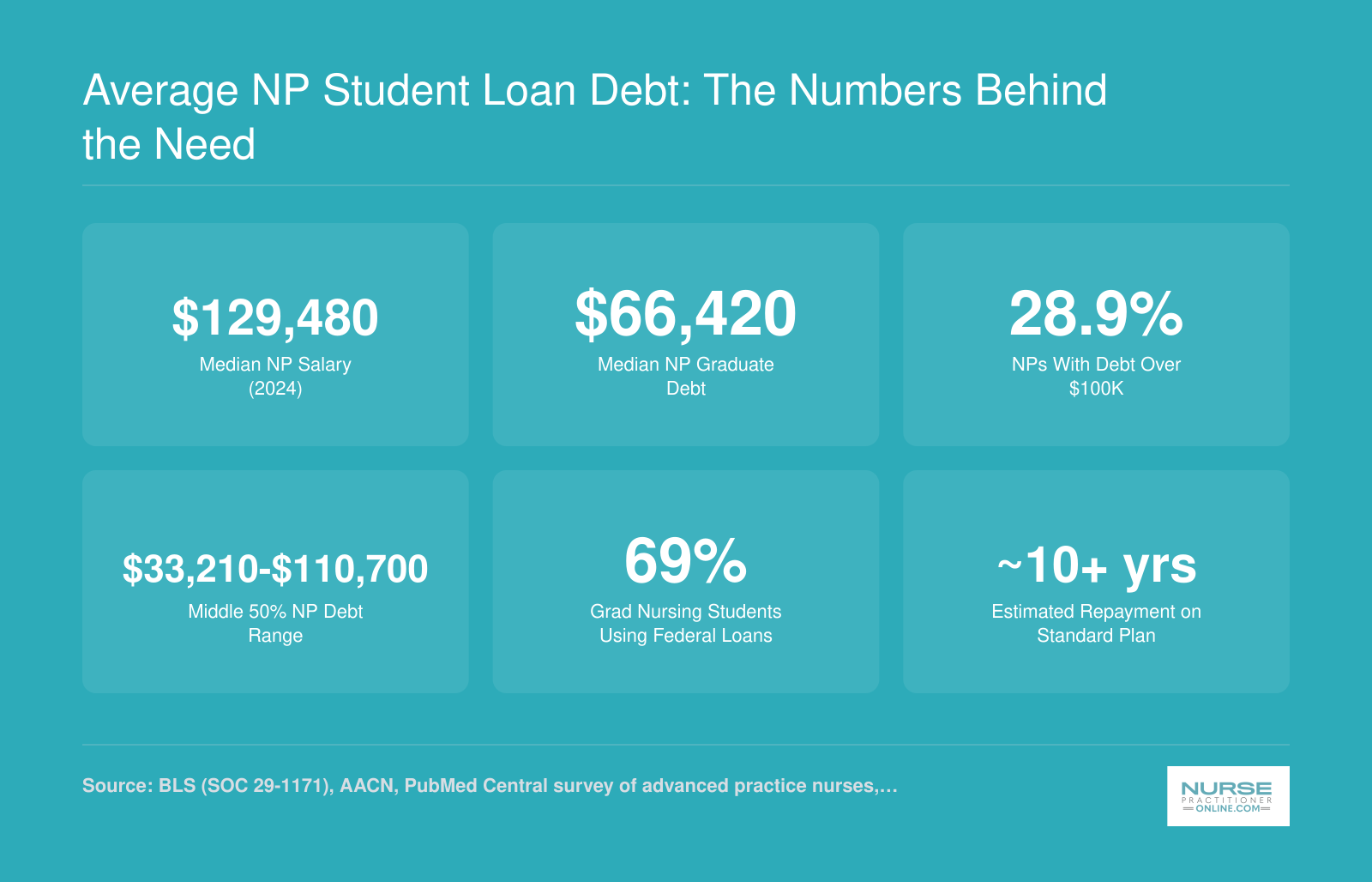

Nurse practitioner programs typically saddle graduates with between $50,000 and $115,000 in student loan debt, depending on whether they enter through an online MSN NP program or DNP pathway and whether they carry prior RN debt. That figure represents one to two years of pre-tax income for many early-career NPs, and under standard ten-year repayment, monthly payments can consume 15 to 20 percent of take-home pay.

The good news: nurse practitioners qualify for multiple federal and state loan forgiveness and repayment programs specifically designed to reduce that burden in exchange for service in underserved communities or at qualifying employers. The four major categories are Public Service Loan Forgiveness, the NHSC Loan Repayment Program, the Nurse Corps Loan Repayment Program, and state-based repayment initiatives. Each carries different eligibility rules, service commitments, award amounts, and tax consequences.

The right combination depends on where you work, how much flexibility you have to relocate, and whether your employer qualifies as a nonprofit or public entity. Some NPs eliminate their entire balance through PSLF after ten years, while others collect upfront awards of $50,000 or more through service programs and finish paying off remaining debt ahead of schedule.

How NP Loan Forgiveness and Loan Repayment Programs Work

Nurse practitioners have access to two fundamentally different categories of student debt relief, and understanding the distinction between them is the first step toward choosing the right strategy for your situation.

Loan Forgiveness vs. Loan Repayment: Know the Difference

Loan forgiveness programs eliminate your remaining balance after you complete a specified number of qualifying payments. Public Service Loan Forgiveness (PSLF) is the most prominent example: work full-time for a qualifying nonprofit or government employer, make 120 qualifying monthly payments on an income-driven repayment (IDR) plan, and the federal government forgives whatever balance remains. You continue paying your regular monthly bill throughout the entire ten-year period, then receive forgiveness at the end.

Loan repayment programs work differently. They provide lump-sum awards that pay down your principal directly, in exchange for a multi-year service commitment in a high-need area. The National Health Service Corps (NHSC), Nurse Corps, and most state programs fall into this category. Instead of waiting a decade, you might receive $50,000 toward your loans after completing a two-year contract at a qualifying clinic. The trade-off is that you must work in a designated underserved location, often in a medically underserved area or facility.

PSLF Is Absolutely Available to Nurse Practitioners

A persistent myth claims that PSLF is reserved for doctors, lawyers, or public school teachers. That is categorically false. Nursing qualifies for PSLF as long as you meet three requirements: you work full-time for a 501(c)(3) nonprofit or government entity, you hold Direct Loans (or consolidate other federal loans into the Direct program), and you repay under an income-driven plan. Thousands of nurse practitioners at nonprofit hospitals, community health centers, and public clinics have successfully received PSLF forgiveness since the program's fixes in 2021.

Service Commitments and Geography

Loan repayment programs deliver faster relief but constrain where you practice. NHSC and Nurse Corps require two to three years of full-time service at approved sites, typically federally qualified health centers (FQHCs), rural health clinics, or Indian Health Service facilities. State programs mirror this structure. PSLF, by contrast, lets you work at any qualifying nonprofit or government employer anywhere in the country, offering geographic flexibility in exchange for a longer timeline.

Loan Type Gatekeeping: What Each Program Accepts

PSLF is strict: only federal Direct Loans count. If you hold older FFEL or Perkins loans, you must consolidate them into a Direct Consolidation Loan first, which restarts your 120-payment clock. NHSC and Nurse Corps are more permissive, covering most federal education loans and even some private educational loans used for nursing school, making them viable for NPs whose debt mix includes non-federal financing.

Average NP Student Loan Debt: The Numbers Behind the Need

Even with a strong median salary, nurse practitioners often carry substantial graduate debt that can take years to pay off under standard repayment plans. These figures illustrate why loan forgiveness programs are not just helpful but financially significant for many NPs.

Federal Loan Forgiveness Programs for Nurse Practitioners

Federal loan forgiveness programs for nurse practitioners are government-funded initiatives that eliminate a portion or all of your student loan debt in exchange for service in areas with limited healthcare access. These programs represent some of the most substantial debt relief options available to NPs, with potential awards reaching well into six figures over a full service commitment.

National Health Service Corps Loan Repayment Program

The National Health Service Corps (NHSC) Loan Repayment Program stands as one of the most generous options for nurse practitioners willing to work in underserved communities. Through this program, NPs commit to practicing in federally designated Health Professional Shortage Areas, and in return, HRSA provides tax-free funds applied directly to qualifying educational loans.

The program operates on a tiered structure based on the shortage severity of your practice location. Sites receive HPSA scores ranging from 0 to 26, with higher scores indicating greater need. To qualify for NHSC loan repayment, your practice site must meet minimum score thresholds established each application cycle. Full-time participants typically commit to two or three years of service, with options to extend for additional awards.

Application windows generally open in early spring each year, though exact dates shift annually. Award amounts have seen adjustments over recent cycles, so verifying current caps against the official HRSA program pages is essential before making service commitment decisions.

Nurse Corps Loan Repayment Program

The Nurse Corps Loan Repayment Program specifically targets registered nurses, advanced practice registered nurses, and nurse faculty. For nurse practitioners, this program requires employment at eligible facilities experiencing critical nursing shortages, including many community health centers, rural clinics, and safety-net hospitals.

Participants commit to a two-year initial service obligation, with the possibility of extending for a third year. The percentage of loan balance covered varies by year of participation, making longer commitments financially advantageous for those with substantial debt. Beyond individual financial benefits, NPs who advocate for expanded program funding play an important role in shaping nurse practitioner health policy.

Finding Current Program Details

Because award amounts, eligibility thresholds, and application deadlines change annually, relying on outdated information can derail your planning. The most reliable sources include:

- HRSA's official program pages: Visit hrsa.gov and navigate to the specific NHSC Loan Repayment and Nurse Corps Loan Repayment sections for current award caps and application windows.

- HPSA Find tool: The data.hrsa.gov site lets you search HPSA scores for specific facilities and geographic areas, helping you identify qualifying practice locations.

- Professional organizations: The American Association of Nurse Practitioners publishes summary updates on program changes and advocates for expanded funding.

- Direct HRSA contact: For personalized questions about your eligibility or application status, HRSA provides toll-free customer service numbers and email contacts on each program page.

Your academic institution's financial aid office or state nursing association can also help interpret program requirements and connect you with current participants who can share firsthand experiences.

Questions to Ask Yourself

State-Based NP Loan Repayment Programs: A State-By-State Breakdown

Which states offer loan repayment for nurse practitioners? Many nurses don't realize that state governments run some of the most lucrative programs, often with less competition than federal options. These state-level initiatives target providers who commit to working in underserved areas, and NPs are frequently eligible. Here's what you need to know, starting with the states where the most NPs practice.

Top States for NP Practice and Their Loan Repayment Programs

California, Texas, Florida, New York, Georgia, Pennsylvania, Ohio, Illinois, North Carolina, and Arizona together employ the majority of the nation's nurse practitioners. Each of these states has at least one active loan repayment program, though award amounts, service commitments, and application cycles vary widely.

- California: The California State Loan Repayment Program awards up to $50,000 for a two-year service commitment in a designated Health Professional Shortage Area.1 NPs are explicitly eligible, and many FQHCs and rural clinics qualify as practice sites.2 Applications typically open once per year, and funding is competitive, so early preparation helps.

- Other large NP states: Texas and Florida, for example, have well-established state loan repayment programs with similar structures. New York runs the Doctors Across New York program, which also accepts NPs for certain loan repayment awards. However, specific award caps, service durations, and eligibility criteria can change with each funding cycle. To avoid outdated information, always check the program's official website directly.

Spotlight on Especially NP-Friendly State Programs

California's program stands out for its clarity: NPs are listed in the eligible provider types, and award amounts are substantial without requiring a commitment longer than two years. Florida's Nursing Student Loan Forgiveness Program focuses more narrowly on nurses, including advanced practice roles, though awards may be smaller. Texas offers multiple pathways, such as the Physician Education Loan Repayment Program, that sometimes include NPs depending on site designation. If you're open to relocating, comparing these programs is worth the effort.

Stacking State and Federal Benefits

One major advantage of state programs is that many allow you to combine their awards with federal forgiveness like PSLF or NHSC. In some cases, you could receive a state repayment while your PSLF qualifying payments accrue simultaneously. The next section covers stacking strategies in detail, so keep reading if you want to maximize total loan relief.

How to Find Programs in Your State

If you practice in a state not listed here, don't assume you're out of luck. Dozens of state loan repayment programs exist, often administered through state health departments or primary care offices. The HRSA State Loan Repayment Program contacts page is the best starting point: it links to every state's program page and includes key contacts for technical assistance. Even if a program isn't currently funded, legislative changes can restore or expand it, so checking annually is smart.

Related Articles

Can You Stack Programs? Combining PSLF, NHSC, and State Programs

Running programs back-to-back versus running them side-by-side: that distinction is the heart of everything you need to understand about combining loan forgiveness options as a nurse practitioner.

The Short Answer: Yes, But With One Key Caveat

Nurse practitioners can generally participate in the NHSC Loan Repayment Program and work toward PSLF at the same time, provided your employer qualifies for both.1 That is genuinely good news. The catch is that the lump-sum payments NHSC sends directly to your loan servicer on your behalf do not count as qualifying PSLF payments.2 Only the payments you make personally, while working full-time at a qualifying government or 501(c)(3) nonprofit employer, count toward PSLF's 120-payment requirement. So the two programs run in parallel, not in competition, but they are also not adding up toward the same finish line.

This matters for sequencing. If NHSC pays down a significant chunk of your principal, the remaining balance you are working toward under PSLF is smaller. That is a real financial advantage, even if the NHSC payments do not directly shorten your PSLF clock.

How to Think About Sequencing

If your employer qualifies for both programs simultaneously, the concurrent approach works well: NHSC reduces your principal while your monthly payments continue to accumulate toward the 120 PSLF qualifying payments. If that is not possible, a sequential strategy still makes sense. Completing an NHSC service commitment first can substantially reduce what you owe, and then you pursue PSLF on the trimmed balance.

One firm limitation to know: NHSC and Nurse Corps Loan Repayment are mutually exclusive during the same service period.3 You can participate in one and then the other, but not both at once. Each NHSC contract covers a single program, so you will need to choose and complete that obligation before moving to the next.4

Layering in State Programs

State loan repayment programs can typically be layered on top of federal programs, though the rules vary by state and program. In practice, it is possible to receive NHSC awards and a state repayment benefit while also accruing PSLF-qualifying payments. Always confirm with your state program administrator that there are no exclusivity requirements before assuming you can combine them.

Keep Your Records Separate and Detailed

The most common source of confusion when stacking programs is losing track of which payments count toward which goal. Keep a running log of your PSLF-qualifying payment count entirely separate from any records of repayment program disbursements. The PSLF servicer and your repayment program administrator are different entities, and neither will automatically reconcile the other's records for you. Submitting your PSLF Employment Certification Form annually is the simplest way to stay on top of your qualifying payment count so there are no surprises near the finish line.

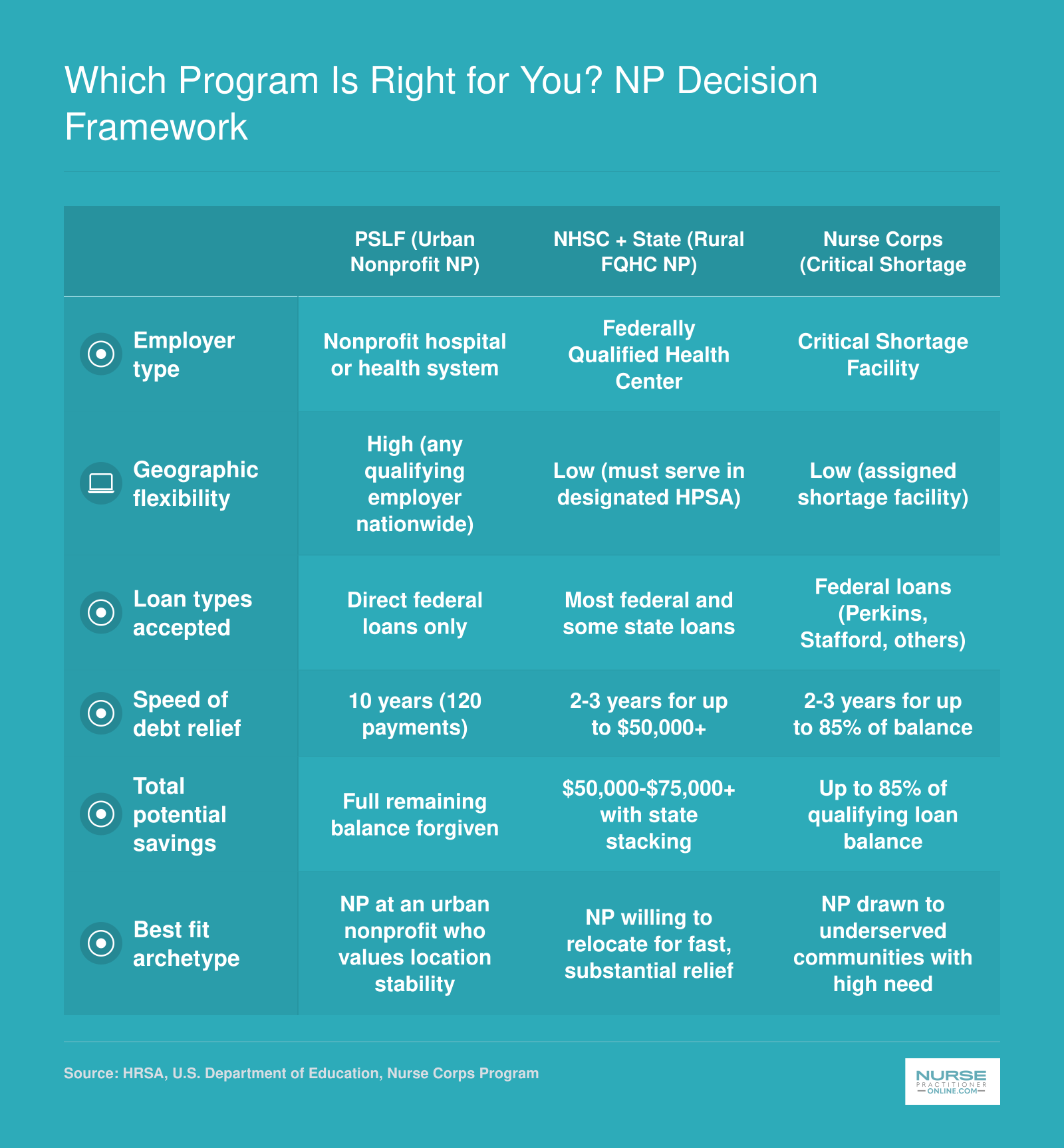

Which Program Is Right for You? NP Decision Framework

Not every forgiveness program fits every nurse practitioner's career path. The right choice depends on where you work, how quickly you need relief, and whether you're open to relocating. Use this framework to match your situation to the strongest program option.

How Much Will You Actually Save? NP Forgiveness Scenarios

$80,000 in student loan debt sounds daunting, but the right forgiveness strategy can eliminate tens of thousands of dollars from your repayment total. Let's walk through three realistic scenarios showing how different programs translate into real savings for nurse practitioners at various debt levels.

Scenario 1: PSLF Only with $80K Debt

Consider an NP earning $120,000 annually with $80,000 in federal student loans who works full-time at a nonprofit hospital. Under the PAYE or new IBR plan, monthly payments are calculated at 10% of discretionary income, which is your adjusted gross income minus 150% of the federal poverty level.1

For this NP, the estimated monthly payment comes to approximately $718 per month.2 Over 10 years of qualifying payments under PSLF, that totals roughly $86,160 paid. However, if this debt accrued substantial interest during school and residency, the remaining balance at forgiveness could still exceed $40,000 to $50,000 depending on the original interest rate and any capitalization events.

The key insight here is that PSLF works best when your debt is high relative to your income. An NP with $150,000 in debt at the same salary would pay the same monthly amount but have far more forgiven at the 10-year mark.

Scenario 2: NHSC Plus PSLF with $100K Debt

Now consider an NP with $100,000 in debt who secures an NHSC Loan Repayment Program award. With a two-year initial service commitment at a qualifying HPSA site, this NP receives up to $50,000 in direct loan repayment from NHSC.

Here's where stacking becomes powerful. During those same two years, the NP makes IDR payments that count toward PSLF. After the NHSC commitment ends, the remaining $50,000 balance continues accruing PSLF-qualifying payments if the NP stays at a nonprofit or public employer.

By year 10, assuming continued qualifying employment, the NP has received $50,000 from NHSC, made approximately $86,160 in IDR payments, and had any remaining balance forgiven through PSLF. Combined savings compared to standard repayment could exceed $60,000 to $80,000 depending on interest accumulation and income changes.

Scenario 3: Nurse Corps with $60K Debt

For an NP with moderate debt of $60,000, the Nurse Corps Loan Repayment Program offers a faster path. The program pays 85% of qualifying nursing education debt over a three-year service period at a Critical Shortage Facility.

85% of $60,000 equals $51,000 in direct repayment, leaving just $9,000 remaining. This NP finishes loan repayment in roughly three years rather than 10, with significantly less paid out-of-pocket compared to either standard repayment or PSLF.

Which Approach Saves You the Most?

PSLF delivers the highest total forgiveness for NPs carrying substantial debt while earning salaries on the lower end for the profession. Think community health NPs, psychiatric NPs at nonprofit clinics, or those working in academic medical centers. (Curious how pay varies? Check out NP specialties by salary.) The monthly payment stays manageable regardless of how large the balance grows.

NHSC and Nurse Corps, by contrast, offer faster relief for moderate debt loads. If you owe $50,000 to $75,000 and can commit to underserved practice, these programs may eliminate your debt years sooner than PSLF.

How Your IDR Plan Choice Affects Savings

Under PAYE and the newer version of IBR, payments are set at 10% of discretionary income.1 The older IBR formula uses 15%, which means significantly higher monthly payments for the same income level. For an NP earning $120,000, that difference is approximately $718 per month under PAYE or new IBR versus roughly $1,076 under old IBR.

Choosing the lower-payment plan maximizes forgiveness under PSLF since you pay less over 10 years before the remaining balance is forgiven. Note that the SAVE Plan is no longer available as of 2026, so PAYE or new IBR are currently your best options for minimizing payments.4

Important Caveats

These scenarios are illustrative starting points, not personalized projections. Your actual savings depend on several variables: income changes over your career, family size affecting your poverty level calculation, the interest rate on your loans, whether you experience periods of unemployment or reduced hours, and whether you successfully gain acceptance into competitive programs like NHSC or Nurse Corps. Running your own numbers with current loan balances and realistic income projections gives you the clearest picture of which path makes financial sense for your situation.

As of mid-2025, nearly 500,000 borrowers have received Public Service Loan Forgiveness, with more than 7.6 billion dollars discharged since the program's overhaul. PSLF is no longer a theoretical promise; it is paying off real debt for real healthcare workers right now.

Tax Implications of NP Loan Forgiveness Programs

Not all loan forgiveness comes with the same tax bill. As of 2026, nurse practitioners face a split landscape: some programs offer permanently tax-free awards, while others now trigger federal income taxes that can erase a substantial portion of your forgiveness benefit.

PSLF and Federal Service Programs Remain Tax-Free

Public Service Loan Forgiveness remains tax-free in 2026 and always has been.1 If you work full-time for a qualifying nonprofit hospital or government health agency and make 120 qualifying payments, the forgiven balance is excluded from your federal taxable income. The same permanent tax exclusion applies to the NHSC Loan Repayment Program and the Nurse Corps Loan Repayment Program under Internal Revenue Code Section 108(f)(4), which exempts awards made for increasing the availability of health services in underserved areas.2 These programs were never subject to the temporary ARPA provision and remain unaffected by its expiration.

The IDR Tax Bomb Is Back

Income-driven repayment forgiveness after 20 or 25 years is now taxable as ordinary income.3 The American Rescue Plan Act temporarily excluded student loan forgiveness from federal income taxes between 2021 and 2025, but that exclusion expired on December 31, 2025, and Congress did not extend it. If you reach the end of your IDR term in 2026 or later and receive forgiveness, the IRS will treat the forgiven amount as taxable income in the year it is discharged. For an NP with $80,000 forgiven, that could mean a federal tax bill of $20,000 or more depending on your bracket. The only exceptions are insolvency (you owe more than you own at the time of discharge) or discharge in bankruptcy, both of which require detailed documentation.

State Programs Vary

Most state health-professional loan repayment programs that meet the IRC Section 108(f)(4) criteria (service in underserved areas) are also tax-free at the federal level as of 2026.2 However, some states tax these awards as income on your state return, and a few states that do not conform to federal tax code may treat even NHSC or Nurse Corps awards as taxable. Check your state's Department of Revenue guidance or consult a tax professional familiar with your state's treatment of educational loan repayment assistance.

Plan Ahead and Get Expert Help

If you are combining multiple programs, relying on IDR forgiveness rather than PSLF, or working in a state with non-conforming tax rules, consult a CPA or enrolled agent who understands student loan forgiveness taxation. The difference between a tax-free award and a taxable discharge can swing your net benefit by tens of thousands of dollars, and planning ahead allows you to save for any tax liability or adjust your forgiveness strategy before it is too late.

Step-By-Step: How to Apply for NP Loan Forgiveness

Applying one month before graduation versus planning during your first semester can mean the difference between seamless enrollment and missing critical deadlines that delay forgiveness by years.

Navigating loan forgiveness isn't a one-time task. It's a multi-year process that rewards organized, proactive nurse practitioners and penalizes those who wait until the finish line to get their paperwork in order. Here's your complete roadmap.

Step 1: Inventory Your Federal Loans

Log into studentaid.gov and pull up your loan portfolio. You need to confirm every loan is a Direct Loan. If you see Federal Family Education Loans (FFEL) or Perkins Loans, those don't qualify for Public Service Loan Forgiveness or most federal programs until you consolidate them into a Direct Consolidation Loan. Consolidation resets your payment count for PSLF, so do this before you make your first qualifying payment, not five years in. Write down your loan servicer, total balance, and loan types. This inventory becomes your baseline.

Step 2: Verify Your Employer's Eligibility

For PSLF, your employer must be a government organization or a 501(c)(3) nonprofit. Ask your HR department for documentation, or search the IRS Tax Exempt Organization Search to confirm nonprofit status. For NHSC or Nurse Corps, your facility must be located in a Health Professional Shortage Area or designated critical shortage facility. Use the HRSA HPSA finder tool to check your work site's designation before you accept a job offer. Don't assume a rural clinic qualifies; verify it.

Step 3: Enroll in an Income-Driven Repayment Plan (for PSLF)

If you're pursuing PSLF, you must be on an IDR plan: SAVE, PAYE, IBR, or ICR. The PSLF Help Tool on studentaid.gov walks you through plan selection and generates the correct forms. Submit your IDR application as soon as you're employed. Your monthly payment amount is based on income and family size, and every qualifying payment counts toward your 120-payment requirement.

Step 4: Submit the PSLF Employer Certification Form Annually

This is the step most borrowers skip and regret. Don't wait ten years to certify your employment. Submit the PSLF form (officially called the Employment Certification Form) every year, or whenever you change jobs. This creates a paper trail that confirms qualifying payments in real time. Use the PSLF Help Tool to generate the form, have your HR department sign it, and upload it through studentaid.gov. Keep a copy in your personal files.

Step 5: Apply to NHSC or Nurse Corps During Open Windows

NHSC and Nurse Corps open applications once a year, typically in spring or early summer, and funding is competitive. Apply early in the cycle. You'll need to commit to a multi-year service obligation at an approved site. Review the application checklist on the NHSC or Nurse Corps websites months in advance. Missing one document can disqualify your application for an entire year.

Create a Loan Forgiveness File and Keep Everything

Open a dedicated folder, physical or digital, for loan forgiveness. Save every Employer Certification Form, NHSC contract, payment confirmation, tax return, and servicer statement. Borrowers who can't produce records when discrepancies arise lose months or years of credit. Set a calendar reminder every January to update your file and submit your annual PSLF certification.

Timeline and Planning

PSLF requires 120 qualifying payments over ten years of full-time nonprofit or government employment. NHSC and Nurse Corps require two- to four-year service commitments with upfront contracts. If you're fresh out of school, start your PSLF clock immediately and consider layering NHSC in your first or second year for maximum benefit. Whether you're still researching how to enroll in NP school online or already in practice, the earlier you start, the more debt you erase.

Frequently Asked Questions About NP Loan Forgiveness

Navigating loan forgiveness as a nurse practitioner can feel overwhelming, especially when you are juggling clinical work, family, and continuing education. Below are answers to the questions NPs ask most often about federal and state forgiveness and repayment options available in 2026.

- Can nurse practitioners get student loan forgiveness?

- Yes. Nurse practitioners qualify for several federal programs, including Public Service Loan Forgiveness (PSLF), the NHSC Loan Repayment Program, and the Nurse Corps Loan Repayment Program. Many states also offer their own repayment assistance for NPs who serve in underserved or high-need areas. The key is meeting each program's specific employment, loan type, and service requirements.

- What is the best loan forgiveness program for nurse practitioners?

- It depends on your situation. PSLF is ideal if you work for a qualifying nonprofit or government employer and can commit to 120 qualifying payments under an income-driven plan. The NHSC program is often better for NPs with large balances who are willing to work at approved shortage sites, because it offers lump-sum repayment in as few as two years. Compare service commitments, award amounts, and timeline before choosing.

- Can you combine PSLF with NHSC or Nurse Corps loan repayment?

- You can, with careful planning. While you receive NHSC or Nurse Corps payments, those payments reduce your loan balance, but the months still count toward your PSLF 120-payment requirement if you also make qualifying payments on the remaining balance. You cannot double-count a single dollar of forgiveness, yet running both programs in parallel can dramatically shorten your repayment timeline and total savings.

- Is loan forgiveness for nurse practitioners taxable?

- Under PSLF, forgiven balances are not treated as taxable income, and that benefit is permanent under federal law. NHSC and Nurse Corps awards are also tax-free at the federal level. However, if you eventually receive forgiveness through an income-driven repayment plan outside of PSLF, the forgiven amount may be taxable after 2025 unless Congress extends the temporary exemption. Always confirm your state's tax treatment as well.

- Do I need to work at an FQHC to qualify for NHSC loan repayment as an NP?

- Not necessarily. Federally Qualified Health Centers (FQHCs) are among the most common approved sites, but the NHSC also recognizes other settings in Health Professional Shortage Areas, including rural health clinics, Indian Health Service facilities, and certain correctional or behavioral health sites. What matters is that the site holds current NHSC approval and is located in or serves a designated shortage area.

- How much student loan debt does the average nurse practitioner have?

- Estimates vary by degree pathway, but many NPs graduate with between $40,000 and $100,000 or more in student loan debt. Those who completed a BSN-to-DNP or post-master's DNP program tend to carry higher balances. High debt loads are a major reason forgiveness and repayment programs are so valuable for NPs pursuing advanced practice careers.

- Does my NP specialty affect which forgiveness programs I qualify for?

- It can. NHSC prioritizes primary care disciplines such as family, adult-gerontology, pediatric, and psychiatric-mental health nurse practitioners. Acute care and certain subspecialty NPs may have fewer options through NHSC but can still qualify for PSLF, Nurse Corps, and many state programs. Psychiatric-mental health NPs are in especially high demand, which can improve your chances of selection in competitive programs.